H. Rates Volatility Modeling: An Overview

[1]:

import IPython; IPython.display.HTML('''<script>code_show=false; function code_toggle() { if (code_show){ $('div.nbinput').show(); } else { $('div.nbinput').hide(); } code_show = !code_show} $( document ).ready(code_toggle);</script><form action="javascript:code_toggle()"><input type="submit" value="Click here to toggle on/off the raw code."></form>''')

[1]:

Agenda

Part I: Vanilla Models

Option Pricing Basics, Binomial Tree

Vanilla Option Pricing Models

SABR

Displaced Lognormal

Change of Numeraire

Applications

Swaption Pricing In SABR

CMS Spread Option Pricing With Copula

Part II: Term Structure Models

HJM Framework, Forward Rate Vol

Hull-White Model

Cheyette

Option Pricing Basics

The Fundamental Principle: In a no-arbitrage market, the price of any derivative with payoff \(X\) is the expectation of its discounted payoff under the risk-neutral measure \(P^M\)

The Universal Formula:

\(M_t\): Time-\(t\) value of the money market account with \(M_0 = 1\) (the numeraire)

\(P^M\): The risk-neutral probability measure associated with \(M\)

\[V_0 = M_0 E^M \left[ M_T^{-1} X_T \right]\]

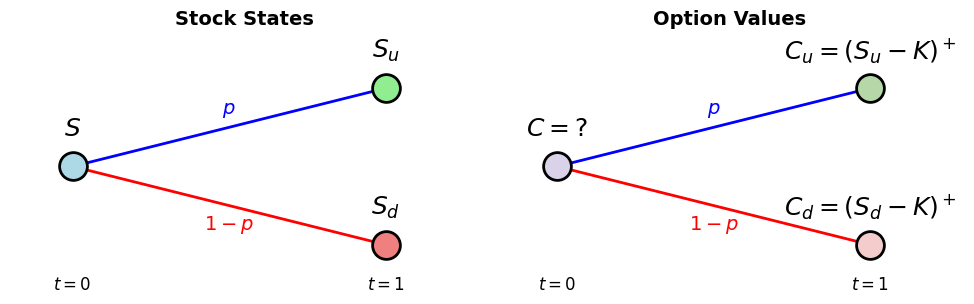

Binomial Option Pricing Model (BOPM)

We want to price an option on a stock trading at \(S\) currently

Assumptions:

Only two discrete times (one time step): Today at \(t=0\) and maturity at \(t=1\)

At \(t=1\), the stock price can either go up to \(S_u\) or go down to \(S_d\) (two states), with corresponding option prices \(C_u\) and \(C_d\), respectively

A money market account (MMA) with initial value 1 will become \(M\) at \(t=1\)

[2]:

# Single-step binomial tree visualization (stock + option payoff tree)

import matplotlib.pyplot as plt

fig, (ax_stock, ax_opt) = plt.subplots(1, 2, figsize=(10, 3.5))

# Shared node positions

t0_x, t0_y = 0, 0.5

t1_u_x, t1_u_y = 1, 0.75

t1_d_x, t1_d_y = 1, 0.25

node_size = 400

# -------- Left panel: stock tree --------

ax_stock.plot([t0_x, t1_u_x], [t0_y, t1_u_y], 'b-', lw=2, label='Up move')

ax_stock.plot([t0_x, t1_d_x], [t0_y, t1_d_y], 'r-', lw=2, label='Down move')

ax_stock.scatter([t0_x], [t0_y], s=node_size, c='lightblue', edgecolors='black', zorder=5, linewidths=2)

ax_stock.scatter([t1_u_x], [t1_u_y], s=node_size, c='lightgreen', edgecolors='black', zorder=5, linewidths=2)

ax_stock.scatter([t1_d_x], [t1_d_y], s=node_size, c='lightcoral', edgecolors='black', zorder=5, linewidths=2)

ax_stock.text(t0_x, t0_y + 0.12, r'$S$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_stock.text(t1_u_x, t1_u_y + 0.12, r'$S_u$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_stock.text(t1_d_x, t1_d_y + 0.12, r'$S_d$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_stock.text(0.5, 0.65, r'$p$', fontsize=14, ha='center', va='bottom', color='blue')

ax_stock.text(0.5, 0.35, r'$1-p$', fontsize=14, ha='center', va='top', color='red')

ax_stock.text(t0_x, 0.15, r'$t=0$', fontsize=12, ha='center', va='top')

ax_stock.text(t1_u_x, 0.15, r'$t=1$', fontsize=12, ha='center', va='top')

ax_stock.set_xlim(-0.2, 1.3)

ax_stock.set_ylim(0.2, 0.9)

ax_stock.set_aspect('equal')

ax_stock.axis('off')

ax_stock.set_title('Stock States', fontsize=14, fontweight='bold', pad=12)

# -------- Right panel: option value tree --------

ax_opt.plot([t0_x, t1_u_x], [t0_y, t1_u_y], 'b-', lw=2)

ax_opt.plot([t0_x, t1_d_x], [t0_y, t1_d_y], 'r-', lw=2)

ax_opt.scatter([t0_x], [t0_y], s=node_size, c='#d9d2e9', edgecolors='black', zorder=5, linewidths=2)

ax_opt.scatter([t1_u_x], [t1_u_y], s=node_size, c='#b6d7a8', edgecolors='black', zorder=5, linewidths=2)

ax_opt.scatter([t1_d_x], [t1_d_y], s=node_size, c='#f4cccc', edgecolors='black', zorder=5, linewidths=2)

ax_opt.text(t0_x, t0_y + 0.12, r'$C=?$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_opt.text(t1_u_x, t1_u_y + 0.12, r'$C_u = (S_u - K)^+$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_opt.text(t1_d_x, t1_d_y + 0.12, r'$C_d = (S_d - K)^+$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_opt.text(0.5, 0.65, r'$p$', fontsize=14, ha='center', va='bottom', color='blue')

ax_opt.text(0.5, 0.35, r'$1-p$', fontsize=14, ha='center', va='top', color='red')

ax_opt.text(t0_x, 0.15, r'$t=0$', fontsize=12, ha='center', va='top')

ax_opt.text(t1_u_x, 0.15, r'$t=1$', fontsize=12, ha='center', va='top')

ax_opt.set_xlim(-0.2, 1.3)

ax_opt.set_ylim(0.2, 0.9)

ax_opt.set_aspect('equal')

ax_opt.axis('off')

ax_opt.set_title('Option Values', fontsize=14, fontweight='bold', pad=12)

# fig.suptitle('One-Step Binomial Trees', fontsize=16, fontweight='bold', y=1.02)

plt.tight_layout()

plt.show()

BOPM No-Arbitrage Argument

Replication Argument:

Set up a portfolio so that its value at \(t=1\) replicates the option in both states

By no-arbitrage, the option price and the portfolio value at \(t=0\) should equal

The portfolio setup at \(t=0\):

Buy \(\Delta {\color{lightgray}~= (C_u - C_d)/(S_u - S_d)}\) shares of the stock at \(S\)

Deposit \(B {\color{lightgray}~= (C_dS_u - C_uS_d)/(M(S_u - S_d))}\) dollars into MMA

It can be easily verified that the portfolio value and option price agree at \(t=1\) in both states: \begin{align*} \Delta S_u + BM &= C_u\\ \Delta S_d + BM &= C_d \end{align*}

Initial portfolio value is \(\Delta S+B\):

\[C = \underbrace{\color{lightgray}\left(\frac{SM - S_d}{S_u - S_d}\right)}_{p^M} \frac{C_u}{M} + \underbrace{\color{lightgray}\left(\frac{S_u - SM}{S_u - S_d}\right)}_{1-p^M} \frac{C_d}{M} = M_0E^M[M^{-1}_T X]\]

Risk-Neutral Probability in BOPM

\(p^M \ne p\) the physical probability which is not in the story

Even if an agent is confident about \(p\), he/she should still quote the option at the fair price \(M_0E^M[M_T^{-1} X]\), as that’s the price to guarantee no arbitrage

Delta Hedge in BOPM

Replicating Portfolio

\(\Delta = (C_u - C_d)/(S_u - S_d)\) shares of the stock at \(S\)

Some MMA (risk free)

\begin{align*} \text{Option} &= \text{Replicating Portfolio}\\ &= \Delta\text{ Shares of Stock} + \text{MMA} \end{align*}

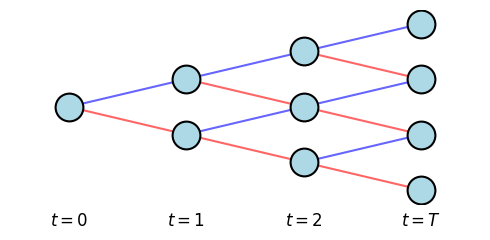

Multi-Step BOPM

Pricing: Construct replicating portfolios at each one-step sub-tree, computing expectations under the risk-neutral probability backward in time from maturity \(T\)

Dynamic Hedging: Compute \(\Delta\) at each node and dynamically rebalance to ensure a locally risk-free portfolio across every time step

[3]:

# 3-step recombining binomial tree visualization

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(5, 2.5))

steps = 3

node_size = 400

# Draw recombining tree nodes and edges

for i in range(steps):

for j in range(i + 1):

# Current node (t=i)

curr_x = i

curr_y = j * 2 - i

# Up move (t=i+1)

up_x = i + 1

up_y = (j + 1) * 2 - (i + 1)

ax.plot([curr_x, up_x], [curr_y, up_y], 'b-', lw=1.5, alpha=0.6)

# Down move (t=i+1)

down_x = i + 1

down_y = j * 2 - (i + 1)

ax.plot([curr_x, down_x], [curr_y, down_y], 'r-', lw=1.5, alpha=0.6)

# Scatter plot for nodes to overlay on top of lines

for i in range(steps + 1):

for j in range(i + 1):

x = i

y = j * 2 - i

ax.scatter(x, y, s=node_size, c='lightblue', edgecolors='black', zorder=5, linewidths=1.5)

# Label each node generically, or using S_... string

# Number of up moves = j, number of down moves = i - j

# ax.text(x, y, f'{j}U\n{i-j}D', fontsize=9, ha='center', va='center', fontweight='bold', zorder=10)

ax.set_xticks(range(steps + 1))

ax.set_xticklabels([f't={i}' for i in range(steps + 1)])

ax.set_yticks([])

ax.set_xlim(-0.5, steps + 0.5)

ax.set_ylim(-steps - 0.5, steps + 0.5)

ax.axis('off')

# Explicitly add time labels at the bottom since axis is off

for i in range(steps):

ax.text(i, -steps - 0.8, f'$t=${i}', fontsize=12, ha='center', va='top')

ax.text(steps, -steps - 0.8, f'$t=T$', fontsize=12, ha='center', va='top')

# ax.set_title('3-Step Recombining Binomial Tree', fontsize=14, fontweight='bold', pad=15)

plt.tight_layout()

plt.show()

With infinitely many time steps, the tree describes a continuous-time stochastic process, and with right assumptions the option price converges to the Black-Scholes formula

Vanilla Option Pricing Models

All we need is a terminal distribution at the expiry \(T\) if our goal is to price/hedge one single vanilla option

Black Normal Model: The underlying (say, a forward rate) follows a scaled Brownian motion

\[dF_t = \sigma\,dW_t \quad\implies\quad F_T\sim N(0, \sigma^2 T),\]which leads to nice closed form formulas

The Reality: Rates are not normally distributed. The market implied distribution has nonzero skewness and excess kurtosis

We need models, like SABR, that parameterize the first 4 moments of the distribution

Implied Volatility: Equating the Black normal formula and the market/model price and back out \(\sigma\)

SABR

\(\alpha\) controls overall level of the implied vol (2nd moment of the distribution)

\(\rho\) controls the implied vol skew (skewness of the distribution, the 3nd moment)

\(\nu\) (vol of vol) controls the implied vol convexity (kurtosis, the 4th moment) \begin{align*} \begin{cases} dF_t = \alpha_tF_t^{\beta}\,dW_t\\ d\alpha_t = {\color{red}\nu} \alpha_t\,dZ_t, \qquad {\color{red}\alpha_0 = \alpha}\\ dW_tdZ_t = {\color{red}\rho} dt \end{cases} \end{align*}

SABR (Cont.)

\(\alpha\) controls overall level of the implied vol (2nd moment of the distribution)

\(\rho\) controls the implied vol skew (skewness of the distribution, the 3nd moment)

\(\nu\) (vol of vol) controls the implied vol convexity (kurtosis, the 4th moment)

[4]:

import numpy as np

def _f_minus_k_ratio(f, k, beta):

"""Hagan's 2002 f minus k ratio - formula (B.67a)."""

eps = 1e-07 # Numerical tolerance for f-k and beta

if abs(f-k) > eps:

if abs(1-beta) > eps:

return (1 - beta) * (f - k) / (f**(1-beta) - k**(1-beta))

else:

return (f - k) / np.log(f / k)

else:

return k**beta

def _zeta_over_x_of_zeta(k, f, t, alpha, beta, rho, volvol):

"""Hagan's 2002 zeta / x(zeta) function - formulas (B.67a)-(B.67b)."""

eps = 1e-07 # Numerical tolerance for zeta

f_av = np.sqrt(f * k)

zeta = volvol * (f - k) / (alpha * f_av**beta)

if abs(zeta) > eps:

return zeta / _x(rho, zeta)

else:

# The ratio converges to 1 when zeta approaches 0

return 1.

def _x(rho, z):

"""Hagan's 2002 x function - formula (B.67b)."""

a = (1 - 2*rho*z + z**2)**.5 + z - rho

b = 1 - rho

return np.log(a / b)

def normal_vol(k, f, t, alpha, beta, rho, volvol):

"""Hagan's 2002 SABR normal vol expansion - formula (B.67a)."""

# We break down the complex formula into simpler sub-components

f_av = np.sqrt(f * k)

A = - beta * (2 - beta) * alpha**2 / (24 * f_av**(2 - 2 * beta))

B = rho * alpha * volvol * beta / (4 * f_av**(1 - beta))

C = (2 - 3 * rho**2) * volvol**2 / 24

FMKR = _f_minus_k_ratio(f, k, beta)

ZXZ = _zeta_over_x_of_zeta(k, f, t, alpha, beta, rho, volvol)

# Aggregate all components into actual formula (B.67a)

v_n = alpha * FMKR * ZXZ * (1 + (A + B + C) * t)

return v_n

[5]:

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import norm

from pandas import DataFrame

from ipywidgets import interact

import warnings

warnings.filterwarnings('ignore')

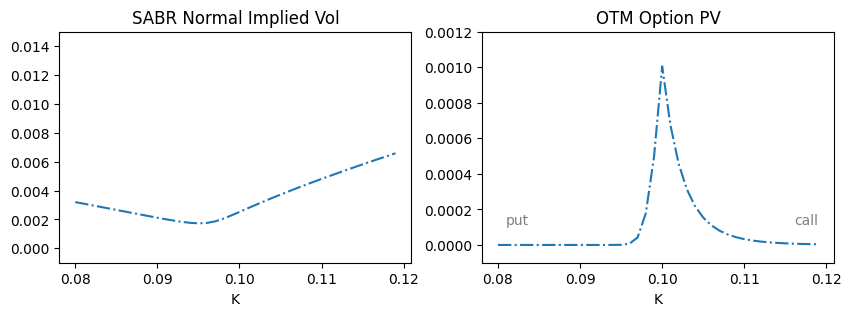

@interact(alpha=(0.001, 0.01, 0.001), rho=(-0.99, 0.99, 0.1), volvol=(0.01, 1, 0.1))

def plot(alpha=0.01, rho=0., volvol=0.6):

beta = 0.6

F = 0.1

T = 1

a = 0.08

b = 0.12

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(10, 3))

def call(K, F, T, A=1):

iv = normal_vol(K, F, T, alpha, beta, rho, volvol)

d = (F-K)/(iv*np.sqrt(T))

return A*iv*np.sqrt(T)*(norm.pdf(d) + d*norm.cdf(d))

def put(K, F, T, A=1):

return call(K, F, T, A) + A*(K-F)

DataFrame([(K, normal_vol(K, F, T, alpha, beta, rho, volvol)) for K in np.arange(a, b, 0.001)], columns=['K', 'Implied Vol']).set_index('K').plot(style='-.', legend=None, ax=ax1)

ax1.set(ylim=(-0.001, 0.015), title='SABR Normal Implied Vol')

DataFrame([(K, call(K, F, T) if K>F else put(K, F, T)) for K in np.arange(a, b, 0.001)], columns=['K', 'OTM Options']).set_index('K').plot(style='-.', legend=None, ax=ax2)

ax2.set(ylim=(-0.0001, 0.0012), title='OTM Option PV')

ax2.text(a + 0.001, 0.0001, 'put', fontsize=10, ha='left', va='bottom', color='gray')

ax2.text(b - 0.001, 0.0001, 'call', fontsize=10, ha='right', va='bottom', color='gray')

plt.show()

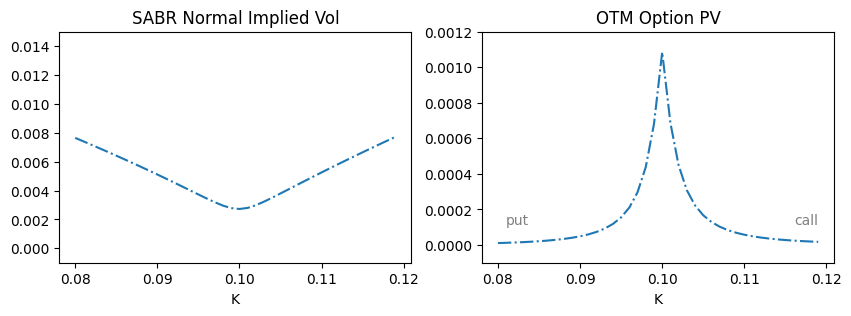

SABR \(\rho\): The Intuition

Why does \(\rho\), the rates vol correlation, control the IV skew?

Consider an OTM call and put at the same absolute moneyness. They are only trading positive because they might become ITM as the underlying moves

When \(\rho \gg 0\) (and vice versa for \(\rho \ll 0\))

Upside Move: Call becomes ITM, the vol increases

Downside Move: Put becomes ITM, the vol decreases

As option value increases with vol, the call is trading higher than the put

[6]:

def plot_static(alpha=0.01, rho=0., volvol=0.6, figusize=(10, 3)):

beta = 0.6

F = 0.1

T = 1

a = 0.08

b = 0.12

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=figusize)

def call(K, F, T, A=1):

iv = normal_vol(K, F, T, alpha, beta, rho, volvol)

d = (F-K)/(iv*np.sqrt(T))

return A*iv*np.sqrt(T)*(norm.pdf(d) + d*norm.cdf(d))

def put(K, F, T, A=1):

return call(K, F, T, A) + A*(K-F)

DataFrame([(K, normal_vol(K, F, T, alpha, beta, rho, volvol)) for K in np.arange(a, b, 0.001)], columns=['K', 'Implied Vol']).set_index('K').plot(style='-.', legend=None, ax=ax1)

ax1.set(ylim=(-0.001, 0.015), title='SABR Normal Implied Vol')

DataFrame([(K, call(K, F, T) if K>F else put(K, F, T)) for K in np.arange(a, b, 0.001)], columns=['K', 'OTM Options']).set_index('K').plot(style='-.', legend=None, ax=ax2)

ax2.set(ylim=(-0.0001, 0.0012), title='OTM Option PV')

ax2.text(a + 0.001, 0.0001, 'put', fontsize=10, ha='left', va='bottom', color='gray')

ax2.text(b - 0.001, 0.0001, 'call', fontsize=10, ha='right', va='bottom', color='gray')

plt.show()

plot_static(rho=0.8)

SABR \(\nu\): The Intuition

The Asymmetric Impact of \(\nu\) (vol of vol) Shocks

Deep (20%) OTM: Requires a vol spike to expire ITM; highly dependent on \(\nu\)

Near-the-Money (1% OTM): Insensitive to \(\nu\); outcome depends on today’s \(\alpha\)

Results

As \(\nu\) goes up, distant tails become more expensive relative to the center

\(\nu\) as the “tail driver”, controls the probability of extreme volatility regimes

[7]:

plot_static(volvol=1, figusize=(10, 3))

Displaced Lognormal Model

An alternative way to parameterize the first 4 moments

Volatility is a linear function of the underlying

\[dF_t = (a_0 + {\color{red}a_1} F_t)\,dW_t\]\({\color{red}a_1}\) controls the IV skew, same as SABR’s \(\rho\):

When \(a_1 > 0\), the vol goes up as the underlying, same as the \(\rho \gg 0\) case (and vice versa for \(a_1 < 0\))

Approximation of the general local volatility model \(dF_t = \sigma(F_t)\,dW_t\) as you can expand \(\sigma(\cdot)\)

Has closed form formulas for NPV and Greeks

Allows negative rates which lognormal does not

Extension to SV gives us a vol of vol parameter \({\color{dodgerblue}\nu}\) to control the convexity of IV, while still preserving semi-closed form formulas

\[\begin{split}\begin{align*} \begin{cases} \color{lightgray}dF_t = {\color{black}\alpha_t}(a_0 + a_1F_t)\,dW_t\\ d\alpha_t = k(\theta - \alpha_t)\,dt + {\color{dodgerblue}\nu}\sqrt{\alpha_t}\,dZ_t \end{cases} \end{align*}\end{split}\]

A Better Parametrization

The displaced lognormal model can be parameterized as

\[dF_t = \sigma( b F_t + (1-b) F_0)\,dW_t\]

Why This Is Better:

For small \(t\) and vol, \(b F_t + (1-b) F_0 \approx F_0\) so \(\sigma\) has the same scale for all values of \(b\)

Parameter Decoupling:

When \(\sigma\) changes, only the IV level changes, not the skew

When \(b\) changes, only the IV skew change, not the level

Extension to SV:

\(\sigma\) can be made a stochastic volatility process, giving us a vol of vol parameter to control the convexity of IV, while still preserving semi-closed form formulas

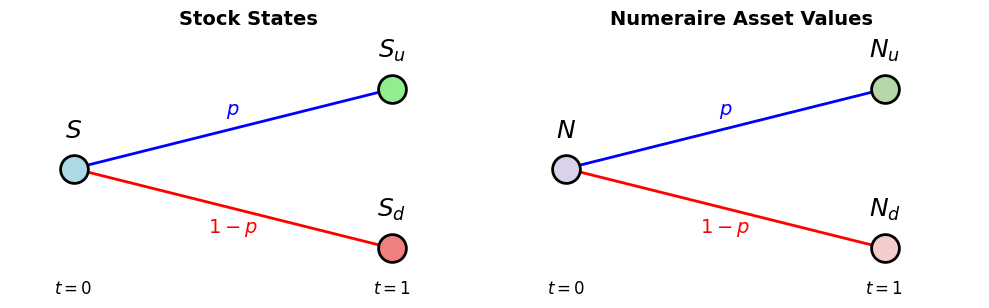

Change of Numeraire

Numeraire: A benchmark asset used as the denominator to price all other assets

Change of Numeraire Formula:

\(N_t\): Time-\(t\) value of the Numeraire

\(P^N\): The probability measure associated with \(N\)

\[V_0 = M_0 E^M \left[ M_T^{-1} X_T \right] = N_0 E^N \left[ N_T^{-1} X_T \right]\]

BOPM With Numeraire Asset

[8]:

# Single-step binomial tree visualization (stock + option payoff tree)

import matplotlib.pyplot as plt

fig, (ax_stock, ax_opt) = plt.subplots(1, 2, figsize=(10, 3.5))

# Shared node positions

t0_x, t0_y = 0, 0.5

t1_u_x, t1_u_y = 1, 0.75

t1_d_x, t1_d_y = 1, 0.25

node_size = 400

# -------- Left panel: stock tree --------

ax_stock.plot([t0_x, t1_u_x], [t0_y, t1_u_y], 'b-', lw=2, label='Up move')

ax_stock.plot([t0_x, t1_d_x], [t0_y, t1_d_y], 'r-', lw=2, label='Down move')

ax_stock.scatter([t0_x], [t0_y], s=node_size, c='lightblue', edgecolors='black', zorder=5, linewidths=2)

ax_stock.scatter([t1_u_x], [t1_u_y], s=node_size, c='lightgreen', edgecolors='black', zorder=5, linewidths=2)

ax_stock.scatter([t1_d_x], [t1_d_y], s=node_size, c='lightcoral', edgecolors='black', zorder=5, linewidths=2)

ax_stock.text(t0_x, t0_y + 0.12, r'$S$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_stock.text(t1_u_x, t1_u_y + 0.12, r'$S_u$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_stock.text(t1_d_x, t1_d_y + 0.12, r'$S_d$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_stock.text(0.5, 0.65, r'$p$', fontsize=14, ha='center', va='bottom', color='blue')

ax_stock.text(0.5, 0.35, r'$1-p$', fontsize=14, ha='center', va='top', color='red')

ax_stock.text(t0_x, 0.15, r'$t=0$', fontsize=12, ha='center', va='top')

ax_stock.text(t1_u_x, 0.15, r'$t=1$', fontsize=12, ha='center', va='top')

ax_stock.set_xlim(-0.2, 1.3)

ax_stock.set_ylim(0.2, 0.9)

ax_stock.set_aspect('equal')

ax_stock.axis('off')

ax_stock.set_title('Stock States', fontsize=14, fontweight='bold', pad=12)

# -------- Right panel: option value tree --------

ax_opt.plot([t0_x, t1_u_x], [t0_y, t1_u_y], 'b-', lw=2)

ax_opt.plot([t0_x, t1_d_x], [t0_y, t1_d_y], 'r-', lw=2)

ax_opt.scatter([t0_x], [t0_y], s=node_size, c='#d9d2e9', edgecolors='black', zorder=5, linewidths=2)

ax_opt.scatter([t1_u_x], [t1_u_y], s=node_size, c='#b6d7a8', edgecolors='black', zorder=5, linewidths=2)

ax_opt.scatter([t1_d_x], [t1_d_y], s=node_size, c='#f4cccc', edgecolors='black', zorder=5, linewidths=2)

ax_opt.text(t0_x, t0_y + 0.12, r'$N$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_opt.text(t1_u_x, t1_u_y + 0.12, r'$N_u$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_opt.text(t1_d_x, t1_d_y + 0.12, r'$N_d$', fontsize=18, ha='center', va='center', fontweight='bold')

ax_opt.text(0.5, 0.65, r'$p$', fontsize=14, ha='center', va='bottom', color='blue')

ax_opt.text(0.5, 0.35, r'$1-p$', fontsize=14, ha='center', va='top', color='red')

ax_opt.text(t0_x, 0.15, r'$t=0$', fontsize=12, ha='center', va='top')

ax_opt.text(t1_u_x, 0.15, r'$t=1$', fontsize=12, ha='center', va='top')

ax_opt.set_xlim(-0.2, 1.3)

ax_opt.set_ylim(0.2, 0.9)

ax_opt.set_aspect('equal')

ax_opt.axis('off')

ax_opt.set_title('Numeraire Asset Values', fontsize=14, fontweight='bold', pad=12)

# fig.suptitle('One-Step Binomial Trees', fontsize=16, fontweight='bold', y=1.02)

plt.tight_layout()

plt.show()

BOPM With Numeraire Asset (Cont.)

If the MMA is replaced by a numeraire asset, the portfolio set up at \(t=0\):

Hold \(h\) share of the stock at \(S\)

Hold \(k\) units of the numeraire asset at \(N\)

Equate the portfolio value and option price at \(t=1\) in both states: \begin{align*} hS_u + kN_u &= C_u\\ hS_d + kN_d &= C_d \end{align*}

Initial portfolio value is \(h S + k N\):

\[C = N\left[\underbrace{\color{lightgray}\left(\frac{SN_uN_d - S_dNN_u}{S_u NN_d - S_d NN_u}\right)}_{p^N} \frac{C_u}{N_u} + \underbrace{\color{lightgray}\left(\frac{-SN_uN_d + S_uNN_d}{S_u NN_d - S_d NN_u}\right)}_{1-p^N} \frac{C_d}{N_d} \right] = N_0E^N[N_T^{-1} X]\]

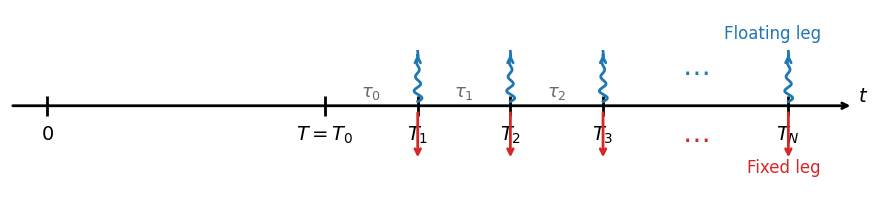

Swaption Pricing

[9]:

def plot_swaption_timeline():

import numpy as np

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(11, 2.5))

# Timeline coordinates

x_t = 0.0

timeline_x = [3.0, 4.0, 5.0, 6.0, 8.0] # T0, T1, T2, T3, TN

labels = [r"$T = T_0$", r"$T_1$", r"$T_2$", r"$T_3$", r"$T_N$"]

# Draw main timeline with arrowhead at the end

ax.annotate("", xy=(8.7, 0), xytext=(-0.4, 0),

arrowprops=dict(arrowstyle="->", color="black", lw=2))

ax.text(8.75, 0.12, r"$t$", ha="left", va="center", fontsize=14)

# Mark today 0

ax.vlines(x_t, -0.12, 0.12, color="black", linewidth=2)

ax.text(x_t, -0.22, r"$0$", ha="center", va="top", fontsize=14)

# Helper to draw a wiggly (floating-leg) arrow

def draw_wiggly_arrow(ax, x, y0=0.05, y1=0.65, amp=0.05, waves=3.5, color="#1f77b4", lw=2):

y = np.linspace(y0, y1, 180)

phase = 2 * np.pi * waves * (y - y0) / (y1 - y0)

taper = np.linspace(1.0, 0.0, y.size)

x_wave = x + amp * np.sin(phase) * taper

ax.plot(x_wave, y, color=color, linewidth=lw)

ax.annotate(

"",

xy=(x, y1),

xytext=(x, y1 - 0.08),

arrowprops=dict(arrowstyle="->", color=color, lw=lw),

)

# Draw all timeline marks and labels

for x, lab in zip(timeline_x, labels):

ax.vlines(x, -0.12, 0.12, color="black", linewidth=2)

ax.text(x, -0.22, lab, ha="center", va="top", fontsize=14)

# Add accrual fractions between T0-T1, T1-T2, T2-T3

tau_midpoints = [3.5, 4.5, 5.5]

tau_labels = [r"$\tau_0$", r"$\tau_1$", r"$\tau_2$"]

for x_tau, tau_lab in zip(tau_midpoints, tau_labels):

ax.text(x_tau, 0.16, tau_lab, ha="center", va="center", fontsize=13, color="dimgray")

# No payments at T0; payments start from T1

payment_dates = timeline_x[1:]

for x in payment_dates:

draw_wiggly_arrow(ax, x)

ax.annotate(

"",

xy=(x, -0.65),

xytext=(x, -0.05),

arrowprops=dict(arrowstyle="->", color="#d62728", lw=2),

)

# Show omitted intermediate payment dates between T3 and TN

ax.text(7.0, 0.40, r"$\cdots$", color="#1f77b4", fontsize=20, ha="center", va="center")

ax.text(7.0, -0.40, r"$\cdots$", color="#d62728", fontsize=20, ha="center", va="center")

# Legend-like labels

ax.text(8.35, 0.80, "Floating leg", color="#1f77b4", ha="right", fontsize=12)

ax.text(8.35, -0.80, "Fixed leg", color="#d62728", ha="right", fontsize=12)

ax.set_xlim(-0.4, 8.8)

ax.set_ylim(-1.15, 1.15)

ax.axis("off")

# ax.set_title("Swaption Cashflow Timeline", fontsize=16, pad=10)

plt.show()

plot_swaption_timeline()

\begin{align*} \text{Time-$t$ Forward Swap NPV} &= \sum_{n=0}^{N-1}\tau_n P(t, T_{n+1})({\color{darkcyan}L(t, T_n, T_{n+1}) \color{red}- K})\\ &= \underbrace{\left(\sum_{n=0}^{N-1}\tau_n P(t, T_{n+1})\right)}_{A(t)}\left(\underbrace{\frac{\sum_{n=0}^{N-1}\tau_n P(t, T_{n+1})L(t, T_n, T_{n+1})}{\sum_{n=0}^{N-1}\tau_n P(t, T_{n+1})}}_{S(t)}- K\right) \end{align*}

Swaption Pricing (Cont.)

Step 1: Change numeraire to the annuity \begin{align*} \text{Payer Swaption NPV } &= M_0E^M[M_T^{-1} {\color{lightgray}(A_T (S_T - K))^+}]\\ &= A_0E^A[A_T^{-1} {\color{lightgray}(A_T (S_T - K))^+}]\\ &= A_0E^A[(S_T - K)^+] \end{align*}

Step 2: Make assumption about \(S_t\) dynamics under the annuity measure, say to follow SABR \begin{align*} \begin{cases} dS_t = \alpha_tS_t^{\beta}\,dW_t^A\\ d\alpha_t = \nu \alpha_t\,dZ_t^A, \qquad \alpha_0 = \alpha\\ dW_t^AdZ_t^A = \rho dt \end{cases} \end{align*} The assumption only gives us \(E^A[(S_T - K)^+]\). We still need to get \(A_0\) from today’s curve

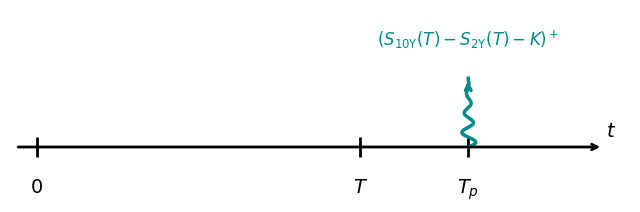

CMS Spread Option Pricing

[10]:

def plot_cms_timeline(cashflow_text=r"$(S_{\text{10Y}}(T) - S_{\text{2Y}}(T) - K)^+$", T_text=r"$T$", direction=1, figsize=(8, 2.5)):

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=figsize)

# Time axis

min_t, max_t = 0, 10

# Draw main timeline with arrowhead at the end

ax.annotate("", xy=(max_t + 0.5, 0), xytext=(-0.4, 0),

arrowprops=dict(arrowstyle="->", color="black", lw=2))

ax.text(max_t + 0.55, 0.12, r"$t$", ha="left", va="center", fontsize=14)

# Markers for t=0, T, T_p

T_val = 6

T_p = 8

ax.vlines(0, -0.07, 0.07, color="black", linewidth=2)

ax.text(0, direction*(-0.22), "$0$", ha='center', va="top", fontsize=14)

ax.vlines(T_val, -0.07, 0.07, color="black", linewidth=2)

ax.text(T_val, direction*(-0.22), T_text, ha='center', va="top", fontsize=14)

ax.vlines(T_p, -0.07, 0.07, color="black", linewidth=2)

ax.text(T_p, direction*(-0.22), "$T_p$", ha='center', va="top", fontsize=14)

# Helper to draw a wiggly (floating-leg) arrow

def draw_wiggly_arrow(ax, x, y0=0.0, y1=0.5, amp=0.15, waves=3.5, color="darkcyan", lw=2.5):

import numpy as np

y = np.linspace(y0, y1, 180)

phase = 2 * np.pi * waves * (y - y0) / (y1 - y0)

taper = np.linspace(1.0, 0.0, y.size)

x_wave = x + amp * np.sin(phase) * taper

ax.plot(x_wave, y, color=color, linewidth=lw)

ax.annotate(

"",

xy=(x, y1),

xytext=(x, y1 - np.sign(y1 - y0) * 0.08),

arrowprops=dict(arrowstyle="->", color=color, lw=lw),

)

# Drawing the cashflow

cashflow_y = direction * 0.5

draw_wiggly_arrow(ax, T_p, y0=0, y1=cashflow_y, amp=0.15, waves=3.5, color="darkcyan", lw=2.5)

ax.text(T_p, cashflow_y + direction * 0.2, cashflow_text,

ha='center', va='bottom', fontsize=12, color="darkcyan")

if direction == 1:

ax.set_ylim(-0.4, 1)

else:

ax.set_ylim(-1, 0.4)

ax.set_xlim(-0.5, max_t + 1)

ax.axis("off")

plt.show()

plot_cms_timeline()

All we need is a distribution \(\color{red}f_{S_{\text{10Y}}, S_{\text{2Y}}}(s_1, s_2)\): \begin{align*} \text{Cash Flow NPV} &= P(0, T_p) E^{T_p}[(S_{\text{10Y}}(T) - S_{\text{2Y}}(T) - K)^+]\\ &= P(0, T_p) \int\int(s_1 - s_2 - K)^+ {\color{red}f_{S_{\text{10Y}}, S_{\text{2Y}}}(s_1, s_2)}\,ds_1ds_2 \end{align*}

If the joint distribution is known in closed form, NPV can be found by numerical integration

Delta Hedging CMS Spread Option

Once we can find NPV \(V\), the spread Delta is the directional derivative of \(V\) along \(\vec u = \frac{1}{\sqrt{2}}(1, -1)\):

\[\frac{\partial V}{\partial (S_1 - S_2)} = \nabla V \cdot u = \frac{\Delta_1 - \Delta_2}{\sqrt{2}},\]where the gradient is

\[\nabla V = \left( \frac{\partial V}{\partial S_1}, \frac{\partial V}{\partial S_2} \right) = (\Delta_1, \Delta_2),\]the single rate Deltas

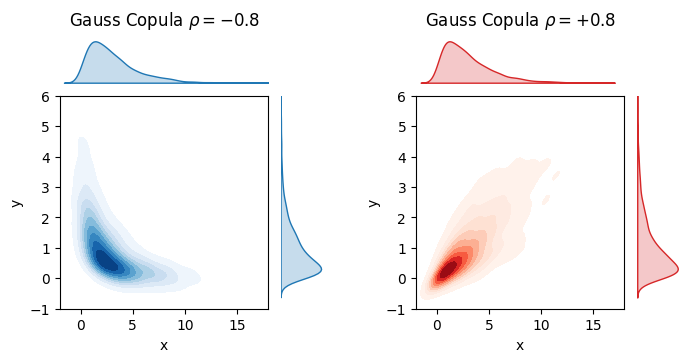

Copula

While \(f_{S_{\text{10Y}}, S_{\text{2Y}}}(s_1, s_2)\) is unknown, its marginal distributions \(f_{S_{\text{10Y}}}(s)\) and \(f_{S_{\text{2Y}}}(s)\) are known (more on this later)

When modeling a joint distribution, copula lets you specify the marginal distributions, while leaving parameters for correlation control

Example with marginal distributions \(\chi^2(3)\) and \(\exp(1)\):

[11]:

from scipy.stats import norm, multivariate_normal, chi2, expon

from pandas import DataFrame

import matplotlib.pyplot as plt

import numpy as np

import seaborn as sns

def plot_data_side_by_side(data1, data2, title1, title2):

'''Plot two joint distributions side-by-side using nested subgridspec to emulate jointplots closely'''

fig = plt.figure(figsize=(8, 3.5))

outer_gs = fig.add_gridspec(1, 2, wspace=0.35)

# --- Panel 1 ---

gs1 = outer_gs[0].subgridspec(5, 5, wspace=0.3, hspace=0.3)

ax1 = fig.add_subplot(gs1[1:5, 0:4])

ax1_x = fig.add_subplot(gs1[0, 0:4], sharex=ax1)

ax1_y = fig.add_subplot(gs1[1:5, 4], sharey=ax1)

ax1_x.axis('off')

ax1_y.axis('off')

sns.kdeplot(x='x', y='y', data=data1, ax=ax1, fill=True, cmap='Blues')

sns.kdeplot(x=data1['x'], ax=ax1_x, fill=True, color='tab:blue')

sns.kdeplot(y=data1['y'], ax=ax1_y, fill=True, color='tab:blue')

ax1_x.set_title(title1, pad=10)

# --- Panel 2 ---

gs2 = outer_gs[1].subgridspec(5, 5, wspace=0.3, hspace=0.3)

ax2 = fig.add_subplot(gs2[1:5, 0:4], sharex=ax1, sharey=ax1)

ax2_x = fig.add_subplot(gs2[0, 0:4], sharex=ax2)

ax2_y = fig.add_subplot(gs2[1:5, 4], sharey=ax2)

ax2_x.axis('off')

ax2_y.axis('off')

sns.kdeplot(x='x', y='y', data=data2, ax=ax2, fill=True, cmap='Reds')

sns.kdeplot(x=data2['x'], ax=ax2_x, fill=True, color='tab:red')

sns.kdeplot(y=data2['y'], ax=ax2_y, fill=True, color='tab:red')

ax2_x.set_title(title2, pad=10)

# Remove extra ticks

for ax in [ax1, ax2]:

ax.tick_params(top=False, right=False)

# Set explicit limits with some margin

ax1.set_xlim(-2, 18.0)

ax1.set_ylim(-1, 6)

import warnings

with warnings.catch_warnings():

warnings.simplefilter("ignore", category=UserWarning)

plt.tight_layout()

plt.show()

rho1 = -0.8

rho2 = 0.8

n = 2000

np.random.seed(0)

# First dataset with rho = -0.8

data1 = DataFrame(multivariate_normal(cov=[[1.0, rho1], [rho1, 1.0]]).rvs(n), columns=['x', 'y'])

data1['x'] = chi2(df=3).ppf(norm.cdf(data1['x']))

data1['y'] = expon.ppf(norm.cdf(data1['y']))

# Second dataset with rho = +0.8

data2 = DataFrame(multivariate_normal(cov=[[1.0, rho2], [rho2, 1.0]]).rvs(n), columns=['x', 'y'])

data2['x'] = chi2(df=3).ppf(norm.cdf(data2['x']))

data2['y'] = expon.ppf(norm.cdf(data2['y']))

plot_data_side_by_side(

data1, data2,

title1=rf'Gauss Copula $\rho = {rho1}$',

title2=rf'Gauss Copula $\rho = +{rho2}$'

)

Gauss Copula

Defined as

\[C_\rho(u, v) = N_\rho(N^{-1}(u), N^{-1}(v))\]\(N(x)\) is the standard normal CDF, and \(N^{-1}(u)\) its inverse function

\(N_\rho(x, y)\) is the bivariate normal CDF with covariance matrix

\[\begin{split}\begin{pmatrix} 1 & \rho\\ \rho & 1 \end{pmatrix}\end{split}\]

How to use: It can be shown that the CDF function

\[F_{X, Y}(x, y) = C_{\color{red}\rho}({\color{dodgerblue}F_X(x), F_Y(y)})\]has marginal CDFs \(F_X(y)\) and \(F_Y(y)\)

Copula lets you specify the marginal distributions, while leaving parameters for correlation control, which we will calibrate to the market

What About Marginal Distributions?

We need CMS rate distribution in the \(T_p\) forward measure, but we only have it in the annuity measure (from SABR), there needs to be an adjustment

Let’s just look at one single CMS rate: Why is there an adjustment?

[12]:

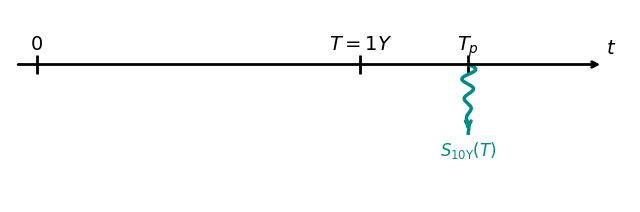

plot_cms_timeline(cashflow_text=r"$S_{\text{10Y}}(T)$", T_text=r"$T=1Y$", direction=-1)

CMS Convexity Adjustment: The Intuition

If you are obligated to pay \(S_{\text{10Y}}\), you’d natually hedge the obligation with a 10Y payer swap

At \(t=0\), set up the hedged portfolio

\[\underbrace{-P(0, T_p) S_{\text{10Y}}(0)}_{\text{CMS}} + h \underbrace{A(0) S_{\text{10Y}}(0)}_{\text{Vanilla Swap}}, \qquad h=\frac{P(0, T_p)}{A(0)}\]When rates rise

The discount factor \(P(0, T_p)\) drops but \(A(0)\) drops more, as it has a longer duration

To rebalance, buy more swap

When rates fall

The discount factor \(P(0, T_p)\) goes up but \(A(0)\) goes up more

Sell some swap

The adjustment is the cost constantly buy payer swaps at high rates and sell at low

Convexity Adjusted CMS Rate

The formula:

\[E^{T_p}[S(T)] = \frac{A(0)}{P(0, T_p)} E^A\left[\frac{P(T, T_p)}{A(T)} S(T)\right]\]

Recall the change of numeraire formula:

\[M_0 E^M [ \underbrace{M_T^{-1} X_T}_{Y} ] = N_0 E^N \left[ N_T^{-1} X_T \right]\]

Set \(Y = M_T^{-1} X_T\) and divide through by \(M_0\):

\[E^M \left[ Y \right] = \frac{N_0}{M_0} E^N \left[ \frac{M_T}{N_T} Y \right]\]

Convexity Adjusted CMS Rate Distribution

Convexity Adjusted CMS Rate:

\[E^{T_p}[S(T)] = \frac{A(0)}{P(0, T_p)} E^A\left[{\color{dodgerblue}\frac{P(T, T_p)}{A(T)}} S(T)\right]\]Write \(P(T, T_p)/A(T)\) as a function of \(S(T)\), known as the annuity mapping function:

\[{\color{dodgerblue}\alpha(S(T)) = \frac{P(T, T_p)}{A(T)}}\]and thus

\[E^{T_p}[S(T)] = \frac{A(0)}{P(0, T_p)} E^A\left[{\color{dodgerblue}\alpha(S(T))} S(T)\right]\]

Convexity Adjusted CMS Rate Distribution:

\[f^{T_p}_{S(T)}(s) = \frac{A(0)}{P(0, T_p)} {\color{dodgerblue}\alpha(s)} \underbrace{f^{A}_{S(T)}(s)}_{\text{from SABR}}\]

Delta-Neutral Break

No directional movement for a few minutes

Agenda

Part II: Term Structure Models

HJM Framework, Forward Rate Vol

Hull-White Model

Cheyette

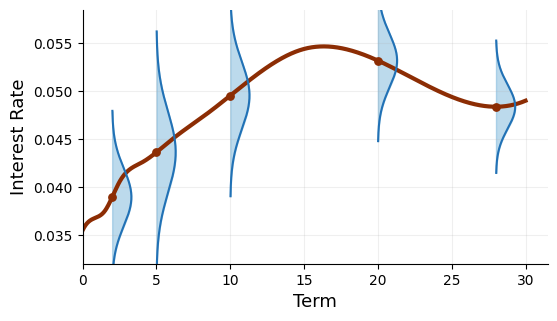

Term Structure Models

In a rates exotics desk, we manage the joint movement of the entire curve

The Challenge: We need one single model to parameterize the first 4 moments of distribution not just at one point, but the entire yield curve

[13]:

def plot_forward_curve_with_vols(figsize=(6, 3.3)):

import numpy as np

import matplotlib.pyplot as plt

from scipy.interpolate import CubicSpline

fwd_knots = np.array([0.0, 0.5, 1.5, 2.5, 4.0, 6.0, 8.5, 15.0, 25.0, 30.0])

fwd_vals = np.array([0.0355, 0.0365, 0.0375, 0.04055, 0.04255, 0.0449, 0.04773, 0.0544, 0.0494, 0.0490])

cs = CubicSpline(fwd_knots, fwd_vals, bc_type='not-a-knot')

maturity = np.linspace(0, 30, 1201)

forward_curve = cs(maturity)

fig, ax = plt.subplots(figsize=figsize)

ax.plot(maturity, forward_curve, color='#8c2d04', linewidth=3)

pillars = np.array([2, 5, 10, 20, 28], dtype=float)

pillar_forwards = cs(pillars)

vols = np.array([0.0030, 0.0042, 0.0035, 0.0028, 0.0023])

width_scale = 1.3

for pillar, center, vol in zip(pillars, pillar_forwards, vols):

move = np.linspace(-3 * vol, 3 * vol, 250)

density = np.exp(-0.5 * (move / vol) ** 2)

density /= density.max()

x_right = pillar + width_scale * density

ax.fill_betweenx(center + move, pillar, x_right, color='#6baed6', alpha=0.45)

ax.plot(x_right, center + move, color='#2171b5', linewidth=1.5)

ax.scatter([pillar], [center], color='#8c2d04', s=28, zorder=3)

ax.set_xlim(0, 31.5)

ax.set_ylim(0.032, 0.0585)

ax.set_xlabel('Term', fontsize=13)

ax.set_ylabel('Interest Rate', fontsize=13)

ax.grid(alpha=0.2)

for spine in ['top', 'right']:

ax.spines[spine].set_visible(False)

plt.show()

plot_forward_curve_with_vols()

Heath–Jarrow–Morton (HJM) Framework

Under the risk-neutral probability, once forward rate vol is determined, so is its drift

\(f(t, T)\): Instantaneous forward rate for the reference period \([T, T+\epsilon]\) observed at \(t\)

\(\sigma(t, T)\): Forward rate vol

\({\color{lightgray}\Sigma(t, T) = \int_t^T\sigma(t, u)\,du: \text{zero coupon bond vol}}\)

\[df(t, T) = {\color{lightgray} \sigma(t, T)\Sigma(t, T)\,dt} + \sigma(t, T)\,d\widetilde W(t), \qquad t<T\]

[14]:

plot_forward_curve_with_vols(figsize=(5, 1.5))

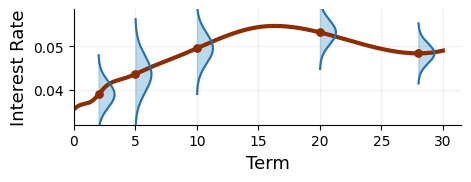

Think of a fixed \(T\), say 10Y

\[df_{\text{10Y}}(t) = {\color{lightgray} \sigma_{\text{10Y}}(t)\Sigma_{\text{10Y}}(t)\,dt} + \sigma_{\text{10Y}}(t)\,d\widetilde W(t), \qquad t<\text{10Y}\]

HJM Is Not Optional

To guarantee no arbitrage, any model for the instantaneous forward rate must have the drift term in the form as specified in the HJM framework

But if you don’t model instantaneous forward rate, then HJM is irrelevant

An example is the LIBOR Market Model

We only have to specify a \(\sigma(t, T)\) to obtain a concrete HJM model for pricing and hedging

So how can we specify a \(\sigma(t, T)\)? Some properties:

Separable

Time stationary

Deterministic

Separable Vol

A special class of HJM models where the volatility function is in the form

\[\sigma(t, T) = g(t)h(T)\]Why does it matter?

In an HJM model with separable vol, the forward rate is Markovian

Markov Process: A random process’s future state only depends on its current state, not the past

Markovian example:

\[E[X_{t+1}|\mathcal F_t] = E[X_{t+1}|X_t]\]Non-Markovian example:

\[E[X_{t+1}|\mathcal F_t] = E[X_{t+1}~|~X_t, X_{t-1}, X_{t-2}]\]

Non-Markovian rates are path-dependent: dynamic hedging is infeasible, pricing is computationally explosive, and rate predictability opens the door to statistical arbitrage

Time Stationary Vol

If the forward rate vol is a function of \(\tau = (T-t)\), we say it’s time stationary

Why does it matter?

Today’s 10Y forward rate vol is \(\sigma(0, 10)\)

1M from now, the same model gives the 10Y forward rate vol \(\sigma(\frac{1}{12}, 10 + \frac{1}{12})\)

When \(\sigma(t, T)\) is time stationary, they are the same

\(\tau = (T-t)\) is the term in a term structure model

Time stationary vol means the vol stays constant for the same term when time \(t\) moves forward

Without further information, time stationary vol is a good assumption

Gaussian HJM Model

Assume that \(\sigma(t, T)\) is deterministic, giving normally distributed forward rates

\[f(t, T) = {\color{lightgray} f(0, T) + \int_0^t\sigma(s, T)\Sigma(s, T)\,ds} + \int_0^t\sigma(s, T)\,d\widetilde W(s), \qquad t<T\]Examples:

Hull-White One Factor (HW1F)

\[\sigma(t, T) = \sigma e^{-k(T-t)} = \sigma e^{-k\tau}\]Ho-Lee: Constant forward rate vol, special case of HW1F with \(k\downarrow 0\)

\[\sigma(t, T) = \sigma\]

It can be shown that the only HJM model with separable, time stationary and deterministic vol is the Hull-White model (HWNF)

Curve Movement in the Ho-Lee Model

Given \(\sigma(t, T) = \sigma\), at time \(t=0\), the forward rate evolves as \begin{align*} df(t, T) &= \sigma^2T\,dt + \sigma \,d\widetilde W(t) \\ &\approx {\color{darkcyan}\sigma^2\tau\Delta t} + {\color{red}\sigma (\widetilde W(\Delta t))} \end{align*}

\(df(t, T)\) (as a function of \(T\)): Tomorrow’s forward curve movement

\({\color{darkcyan}\sigma^2\tau\Delta t}\): An upward-sloping straight line, deterministic curve steepening

\({\color{red}\sigma (\widetilde W(\Delta t))}\): Perfect parallel shift with random magnitude

The Ho-Lee model implies that the curve is always steepening, albeit by a very small amount

HW1F

With \(\sigma(t, T) = \sigma e^{-\kappa \tau}\), the forward rate evolves as \begin{align*} df(t, T) &= {\color{lightgray}\sigma(t, T)\Sigma(t, T)\,dt} + \sigma(t, T)\,d\widetilde W(t)\\ &= {\color{lightgray}\left(y(t) - kx(t) + \frac{1-e^{-k\tau}}{k} (\sigma^2 - 2ky(t))\right)\,dt} + \sigma e^{-k\tau}\,d\widetilde W(t), \end{align*} where \({\color{lightgray}x(0) = y(0) = 0,}\) \begin{align*} {\color{lightgray} \begin{cases} dx(t) = (y(t) - \kappa x(t))dt + \sigma d\widetilde W(t)\\ dy(t) = (\sigma^2 - 2\kappa y(t)) dt \end{cases}. } \end{align*} The ODE of \({\color{lightgray}y(t)}\) can be solved explicitly to obtain

and the state variable \(x(t)\) is normally distributed.

Curve Movement in HW1F

At \(t=0\), tomorrow’s curve movement is \begin{align*} df(t, T) \approx \underbrace{\frac{\sigma^2(1-e^{-k\tau})}{k} \Delta t}_{\color{dodgerblue}(1)} + \underbrace{\sigma e^{-k\tau} \widetilde W(\Delta t)}_{\color{red}(2)} \end{align*}

\({\color{red}(1)}\): Deterministic curve steepening

\({\color{dodgerblue}(2)}\): Curve movement with random magnitude (\(\widetilde W(\Delta t) = \sqrt{\Delta t}Z\) below)

[ ]:

import numpy as np

import matplotlib.pyplot as plt

from ipywidgets import interact

import warnings

warnings.filterwarnings('ignore')

tau = np.linspace(0, 20, 1000)

@interact(sigma=(0.01, 0.5, 0.01), k=(0.01, 1, 0.01), Z=(-3, 3, 0.1))

def plot_curve_movement(sigma=0.2, k=0.4, Z=-1):

s = sigma

dt = 1/365

drift = (s**2) * (1 - np.exp(-k * tau)) * dt / k

diffusion = s * np.sqrt(dt) * np.exp(-k * tau) * Z

total_movement = drift + diffusion

fig, (ax1, ax2, ax3) = plt.subplots(1, 3, figsize=(15, 3.5))

ax1.plot(tau, drift, linewidth=2, color='darkcyan')

ax1.set_title('(1) Deterministic Steepening', color='darkcyan')

ax1.set_xlim(0, 20)

ax1.set_ylim(-0.1, 0.1)

ax1.grid(True, alpha=0.3)

ax1.set_xlabel(r'$\tau$')

ax1.set_ylabel('Curve Movement')

ax2.plot(tau, diffusion, linewidth=2, color='red')

ax2.set_title('(2) Random Movement', color='red')

ax2.set_xlim(0, 20)

ax2.set_ylim(-0.1, 0.1)

ax2.grid(True, alpha=0.3)

ax2.set_xlabel(r'$\tau$')

ax3.plot(tau, total_movement, linewidth=2, color='blue')

ax3.set_title('Total Curve Movement', color='blue')

ax3.set_xlim(0, 20)

ax3.set_ylim(-0.1, 0.1)

ax3.grid(True, alpha=0.3)

ax3.set_xlabel(r'$\tau$')

plt.tight_layout()

plt.show()

HW2F and PCA

At \(t=0\), tomorrow’s curve movement is \begin{align*} {\small df(t, T) \approx (\text{Deterministic Term}) + \underbrace{\left(\sigma_1 e^{-k_1\tau} + \rho\sigma_2e^{-k_2\tau}\right) \widetilde W_1(\Delta t)}_{\color{red}(1)} + \underbrace{\left(\sigma_2\sqrt{1-\rho^2} e^{-k_2\tau}\right) \widetilde W_2(\Delta t)}_{\color{dodgerblue}(2)}, } \end{align*} where \(\widetilde W_1(\Delta t) \perp\!\!\!\perp \widetilde W_2(\Delta t)\).

\({\color{red}(1)}\): Curve movement contributed by PC1

\({\color{dodgerblue}(2)}\): Curve movement contributed by PC2

Bond Reconstruction Formula

In the Hull-White model, the zero coupon bond (ZCB) price \(P(t, T)\) is known in closed form in terms of the state variable(s)

\[P(t, T) = P(t, T, x_t) {\color{lightgray} = \frac{P(0, T)}{P(0, t)} \exp\left(-G(t, T)x_t - \frac{1}{2}G^2(t, T)y_t\right), }\]where

\[{\color{lightgray} G(t, T) = \frac{1-e^{k(T-t)}}{k}, \qquad y_t = \frac{\sigma^2(1-e^{2kt})}{2k}}\]Why is this useful?

Many important quantities can be written in terms of ZCBs, including:

Forward rate \(L(t, T, T+\tau) = (P(t, T)/P(t, T+\tau) - 1)/\tau\)

Swap rate, as it’s a weighted average of forward rates. We denote this by \(S(t, x_t)\)

Annuity, as it’s a basket of ZCBs. We denote this by \(A(t, x_t)\)

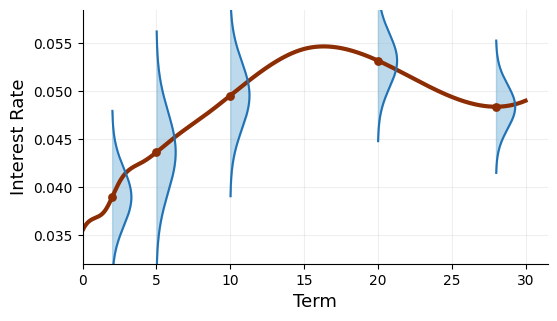

Problem With HW

Despite all the benefits of the Hull-White model, it doesn’t give us control over the 3rd and the 4th moments (IV skews and convexity)

\(f(t, T)\) is normally distributed

The swap rate \(S(t, x_t)\) is not, but there is no parameter for IV skew control

[16]:

plot_forward_curve_with_vols()

From HW to Cheyette

\begin{align*} \begin{cases} dx_t = (y_t - \kappa x_t)dt + {\color{red}\sigma} d\widetilde W_t\\ dy_t = ({\color{red}\sigma}^2 - 2\kappa y_t) dt \end{cases} \end{align*}

HW: Constant \(\sigma\)

Cheyette: \(\sigma(t, x_t, y_t) = a_0 + a_1 x_t\)

Similar to the displaced lognormal model, there is now a skew parameter \(a_1\)

Since \(\sigma\) is random now, so is \(y_t\)

Bond reconstruction formula still holds but with random \(y_t\):

\[P(t, T) = P(t, T, x_t, y_t) {\color{lightgray} = \frac{P(0, T)}{P(0, t)} \exp\left(-G(t, T)x_t - \frac{1}{2}G^2(t, T)y_t\right), }\]where

\[{\color{lightgray} G(t, T) = \frac{1-e^{k(T-t)}}{k}}\]

Cheyette Model With Stochastic Volatility

Extension to SV gives us a vol of vol parameter \({\color{dodgerblue}\nu}\) to control the convexity of IV \begin{align*} \begin{cases} \color{lightgray}dx_t = (y_t - \kappa x_t)dt + {\color{black}\sqrt{\alpha_t}}\sigma(t, x_t, y_t) d\widetilde W_t\\ \color{lightgray}dy_t = ({\color{black}\alpha_t}\sigma^2(t, x_t, y_t) - 2\kappa y_t) dt\\ d\alpha_t = k(\theta - \alpha_t)\,dt + {\color{dodgerblue}\nu}\sqrt{\alpha_t}\,dZ_t \end{cases} \end{align*}

Appendix: Swaption Pricing in Cheyette

Swap rate is now \(S(t, x_t, y_t)\), where \(S(\cdot, \cdot, \cdot)\) is a lengthy formula but in closed form

To find swaption NPV approximation, we find swap rate dynamics approximation: \begin{align*} dS_t &= \frac{\partial S}{\partial x}(t, x_t, y_t)\,dx_t \\ &= \frac{\partial S}{\partial x}(t, x_t, y_t)\sigma(t, x_t, y_t)\,dW^A_t \end{align*}

Replace \(y_t\) by \(\color{red}\bar y_t\), the deterministic function in HW:

\[dS_t \approx \frac{\partial S}{\partial x}(t, x_t, {\color{red}\bar y_t})\sigma(t, x_t, {\color{red}\bar y_t})\,dW^A_t\]The right hand side is in terms of \(x_t\), not \(S_t\), which is undesired

Expand \(S(t, x, y)\) in \(x\) to the first order and find the inverse function as an approximation of \(x(t, S)\). Denote the inverse function by \(\xi(t, s)\). Next write

\[dS_t \approx \underbrace{\frac{\partial S}{\partial x}(t, \xi(t, S_t), \bar y_t)\sigma(t, \xi(t, S_t), \bar y_t)}_{\text{RHS vol}}\,dW^A_t\]

Find first order approximation \(\text{RHS vol} \approx a_0(t) + a_1(t) S_t\). Now we have a swap rate dynamics approximation which is displaced lognormal and can be used in pricing:

\[dS_t \approx (a_0(t) + a_1(t) S_t)\,dW^A_t\]

[17]:

# import numpy as np

# import matplotlib.pyplot as plt

# fig, ax = plt.subplots(figsize=(7, 5))

# # Use y = -T so the T-axis points downward on the page.

# t_max = 10

# T_max = 10

# t = np.linspace(0, t_max, 400)

# y_line = -t

# # Shade the region below the line t = T in the fourth quadrant.

# ax.fill_between(t, y_line, -T_max, color="#9ecae1", alpha=0.6)

# ax.plot(t, y_line, color="#08519c", linewidth=2.5)

# # Clean frame and draw custom axes.

# for spine in ax.spines.values():

# spine.set_visible(False)

# ax.set_xlim(-0.5, t_max + 0.8)

# ax.set_ylim(-T_max - 0.8, 0.8)

# ax.set_xticks([])

# ax.set_yticks([])

# ax.annotate("", xy=(t_max + 0.5, 0), xytext=(0, 0),

# arrowprops=dict(arrowstyle="->", linewidth=2, color="black"))

# ax.annotate("", xy=(0, -T_max - 0.5), xytext=(0, 0),

# arrowprops=dict(arrowstyle="->", linewidth=2, color="black"))

# ax.text(t_max + 0.55, 0.15, r"$t$", fontsize=16)

# ax.text(-0.35, -T_max - 0.55, r"$T$", fontsize=16)

# ax.text(6.2, -5.3, r"$t = T$", color="#08519c", fontsize=14)

# ax.text(6.3, -8.8, "HJM domain", color="#08306b", fontsize=13)

# plt.show()