5. Curve Interpolation

[26]:

from fixedincome2025 import table

What To Do With Missing Points?

When you compute the present value (PV) of your bond portfolio in practice, there will be missing points on the yield curve

Treasury yield curve from treasury.gov:

[27]:

table('yc_09152025')

[27]:

| 1 Mo | 1.5 Mo | 2 Mo | 3 Mo | 4 Mo | 6 Mo | 1 Yr | 2 Yr | 3 Yr | |

|---|---|---|---|---|---|---|---|---|---|

| Yield | 4.22% | 4.21% | 4.17% | 4.06% | 4.00% | 3.81% | 3.64% | 3.54% | 3.50% |

Imagine you have a Treasury bond that’s 11M from its maturity, and the second-to-last coupon payment is 5M from now

You need 5M point and 11M point to price the bond

One also needs to take DCC into consideration when computing the year fractions (\(T\) in the discount factor \(e^{-TR(0, T)}\))

A World of Curves

Although we’ve been using the Treasury yield curve as our only example, in practice there are many other curves

Important ones are SOFR, Term SOFR, fed funds, LIBOR

SOFR is by far the most important one if you work in the rates business in a bank, more important than the Treasury yield curve

In the rates business, many curves are simply a spread curve plus the SOFR curve, spread from basis swap quotes

In a credit desk (trading credit products including corporate bonds), corporate bond yield curves are a spread curve (known as the z-spread) plus the Treasury yield curve

Each curve has its own 6 representations

Below is how a SOFR curve should be interpolated

Curve Interpolation Methods

Curve interpolation is on the time-weighted zero rate \(TR(0, T)\)

The interpolation method is

Linear interpolation in the short end

Cubic spline for the rest

Cutoff is around 3Y, a decision more of an art than science

Why Linear Interpolation on Time-Weighted Zero Rate?

Recall that \begin{align*} f(0, T) &= \frac{\partial }{\partial T} [TR(0, T)] \end{align*}

The reason people use linear interpolation on time-weighted zero rate in the short end is that we want its first derivative, the instantaneous forward curve (\(f(0, T)\) for all \(T\)), to be a step function in the short end

Linear interpolating function: Piecewise linear

Step function: Piecewise constant

The first derivative of a linear interpolating function is a step function

Why Piecewise Constant \(f(0, T)\)?

Recall that

\[L(0, T, T+\tau) = \frac{1}{\tau}\left(e^{\int_T^{T+\tau} f(0, u)\,du} - 1\right)\]A variant of this formula is used to quote FRAs (and swaps)

Recall the CME Term SOFR example

[28]:

table('term_sofr')

[28]:

| Term SOFR 1M | Term SOFR 3M | Term SOFR 6M | Term SOFR 12M | |

|---|---|---|---|---|

| 09-17-2025 | 4.13359 % | 4.02304 % | 3.85385 % | 3.59516 % |

| 09-16-2025 | 4.13584 % | 4.02570 % | 3.85447 % | 3.60384 % |

| 09-15-2025 | 4.14288 % | 4.02330 % | 3.84833 % | 3.60702 % |

Why Piecewise Constant \(f(0, T)\)? (Cont.)

Think of

\[f(0, T) = L(0, T, T+\epsilon)\]for \(\epsilon\) = 1d

Market quote of \(f(0, T)\), like \(L(0, T, T+\tau)\) for arbitrary tenor \(\tau\), is implied by the prices of market instruments and cannot be chosen subjectively

It is not a matter of opinion

Posting an incorrect quote leads to an arbitrage opportunity

\(f(0, T)\) is the market anticipated time-\(T\) (in the future) daily SOFR fixings, which should stay constant between fed rate decisions

The discontinuities are FOMC meeting dates

Linear Interpolation on Time-Weighted Zero Rate

In conclusion, it makes sense for the \(TR(0, T)\) curve to be a linear function between FOMC meetings dates in the short end

The slope of \(TR(0, T)\) at \(T=T^*\) equals \(f(0, T^*)\), which is the anticipated SOFR daily fixing level at \(T^*\)

FOMC meeting schedule is not determined for 3Y out, why not just make the curve continuous and smooth?

Short End Curve Interpolation: Example I

Assuming:

Today’s SOFR yield curve is as below

From the 2M point to the 3M point there will be no FOMC meetings

30/360 DCC

What should the yield be at the 2.5M point?

[29]:

table('yc_sofr_example')

[29]:

| 1 Mo | 1.5 Mo | 2 Mo | 3 Mo | 4 Mo | 6 Mo | 1 Yr | 2 Yr | 3 Yr | |

|---|---|---|---|---|---|---|---|---|---|

| Yield | 4.22% | 4.21% | 4.17% | 4.06% | 4.00% | 3.81% | 3.64% | 3.54% | 3.50% |

Between 2M and 3M, \(TR(0, T)\) must be a linear function, so we have \begin{align*} &\left(\frac{2}{12}\times 4.17\% + \frac{3}{12}\times 4.06\%\right)/2 = \frac{2.5}{12} \times R\\ \end{align*} and hence \(R = 4.104\%\)

Short End Curve Interpolation: Exercise I

Assuming:

Today’s SOFR yield curve is as below

Between the 2M point and the 3M point there will be no FOMC meetings

30/360 DCC

What should the yield be at the 2.333M point?

[30]:

table('yc_sofr_exercise')

[30]:

| 1 Mo | 1.5 Mo | 2 Mo | 3 Mo | 4 Mo | 6 Mo | 1 Yr | 2 Yr | 3 Yr | |

|---|---|---|---|---|---|---|---|---|---|

| Yield | 4.20% | 4.19% | 4.15% | 4.04% | 4.00% | 3.81% | 3.62% | 3.51% | 3.47% |

Short End Curve Interpolation: Answer I

Between 2M and 3M, \(TR(0, T)\) must be a linear function and forward rates are assumed constant, so we have:

Short End Curve Interpolation: Example II

Assuming:

Today’s SOFR yield curve is as below

Between the 1.5M point and the 2M point there will be no FOMC meetings

Between the 3M point and the 3.5M point there will be no FOMC meetings

There is an FOMC meeting at the 2.5M point where the consensus is that the Fed will \(100\%\) cut its rate by 25 bps

SOFR daily rates moves at the same time by the same amount as the fed funds rate

30/360 DCC

What should the yield be at the 3.333M point?

[31]:

table('yc_sofr_example')

[31]:

| 1 Mo | 1.5 Mo | 2 Mo | 3 Mo | 4 Mo | 6 Mo | 1 Yr | 2 Yr | 3 Yr | |

|---|---|---|---|---|---|---|---|---|---|

| Yield | 4.22% | 4.21% | 4.17% | 4.06% | 4.00% | 3.81% | 3.64% | 3.54% | 3.50% |

Short End Curve Interpolation: Example II (Cont.)

[32]:

table('yc_sofr_example')

[32]:

| 1 Mo | 1.5 Mo | 2 Mo | 3 Mo | 4 Mo | 6 Mo | 1 Yr | 2 Yr | 3 Yr | |

|---|---|---|---|---|---|---|---|---|---|

| Yield | 4.22% | 4.21% | 4.17% | 4.06% | 4.00% | 3.81% | 3.64% | 3.54% | 3.50% |

Recall that the slope of \(TR(0, T)\) in the interval [1.5M, 2M] is \(f(0, T)\), the anticipated SOFR daily fixing level in that interval. Numerically, it’s \begin{align*} \frac{2\times 4.17\% - 1.5\times 4.21\%}{0.5} = 4.05\% \end{align*}

Similarly, the slope of \(TR(0, T)\) in the interval [3M, 3.5M] is the anticipated SOFR daily fixings in that interval, which is \(4.05\% - 0.25\% = 3.8\%\)

The slope can also be written in terms of yield at the 3M point and the 3.3333M point as \begin{align*} \frac{3.3333\times R - 3\times 4.06}{0.3333}, \end{align*} which we know should be \(3.8\%\). Thus \(R\) can be backed out to be \(4.034\%\)

Short End Curve Interpolation: Exercise II

Assuming:

Today’s SOFR yield curve is as below

Between the 1.5M point and the 2M point there will be no FOMC meetings

Between the 3M point and the 3.6M point there will be no FOMC meetings

There is an FOMC meeting at the 2.5M point where the consensus is that the Fed will \(100\%\) cut its rate by 25 bps

SOFR daily rates moves at the same time by the same amount as the fed funds rate

30/360 DCC

What should the yield be at the 3.5M point?

[33]:

table('yc_sofr_exercise')

[33]:

| 1 Mo | 1.5 Mo | 2 Mo | 3 Mo | 4 Mo | 6 Mo | 1 Yr | 2 Yr | 3 Yr | |

|---|---|---|---|---|---|---|---|---|---|

| Yield | 4.20% | 4.19% | 4.15% | 4.04% | 4.00% | 3.81% | 3.62% | 3.51% | 3.47% |

Jump Size Always (Multiple of) 25 Bps?

No

Above computation only works if the market is in good agreement on what will happen in the next FOMC meeting

Only in such situation you know the jump size of the step function

When market is not in good agreement, the jump size is an average of participants’ view

[34]:

table('forward_rate_jump_size')

[34]:

| 10/29/2025 | 12/10/2025 | 1/28/2026 | 3/18/2026 | 4/29/2026 | |

|---|---|---|---|---|---|

| Meeting Date | |||||

| Jump Size (bps) | -22.5 | -17.9 | -12.1 | -9.5 | -6.2 |

Is the Market Often in Good Agreement?

Sometimes

When the market is in good agreement, it’s usually only for the next meeting

The meetings after that will be too far

Fed rate decision is driven by unpredictable economic data

inflation, labor market, GDP growth, etc.

Unpredictability of the Economic Data

Weather data is significantly easier to predict than economic data

Weather data: Complex but understood physical processes

Economic data: Unpredictable and irrational human behavior

Economic data is becoming more unpredictable due to

Decline in the quality and reliability of U.S. economic data caused by budget cuts and falling survey response rates

Unexpected global events like pandemics and geopolitical conflicts

Lack of clarity surrounding government policies

Economic uncertainty can harm business investment and hiring, as businesses struggle to plan in a constantly shifting environment

Extrapolation at the Short End

The assumption that \(TR(0, T)\) is piecewise linear leads to flat extrapolation on the left

Let \(T\) be the first (shortest) term where we have a quote. Consider \(t<T\): \begin{align*} tR(0, t) = \frac{t}{T} \times TR(0, T) + \frac{T-t}{T} \times 0 = t R(0, T) \end{align*} Thus

\[R(0, t) = R(0, T) \qquad\forall t\in [0, T]\]In particular, the overnight rate \(R(0, \text{1D}) = R(0, T)\)

What About Long End of the Curve?

For yield curve that’s 3Y away, the same state data \(TR(0, T)\) is used in interpolation

We want forward rate to be continuous and smooth

Smooth means 1st order derivative is continuous \begin{align*} f(0, T) &= \frac{\partial }{\partial T} [TR(0, T)] \end{align*}

We need the \(TR(0, T)\) curve to be continuous and have continuous 1st and 2nd derivatives

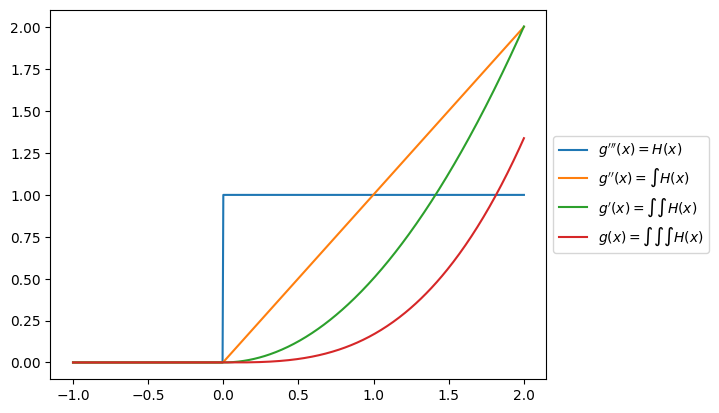

Differentiation and Smoothness

Integrating a piecewise function removes discontinuities

Jumps in the integrand (blue) turn into kinks in the integral (orange)

[35]:

from gfuncpy import gfunc, Identity

@gfunc

def H(x):

if x < 0:

return 0

else:

return 1

x = Identity([-1, 2])

gppp = H(x)

gpp = H(x).int()

gp = H(x).int().int()

g = H(x).int().int().int()

gppp.plot(label=r"$g'''(x) = H(x)$")

gpp.plot(label=r"$g''(x) = \int H(x)$")

gp.plot(label=r"$g'(x) = \int\int H(x)$")

g.plot(label=r"$g(x) = \int\int\int H(x)$")

GFuncPy

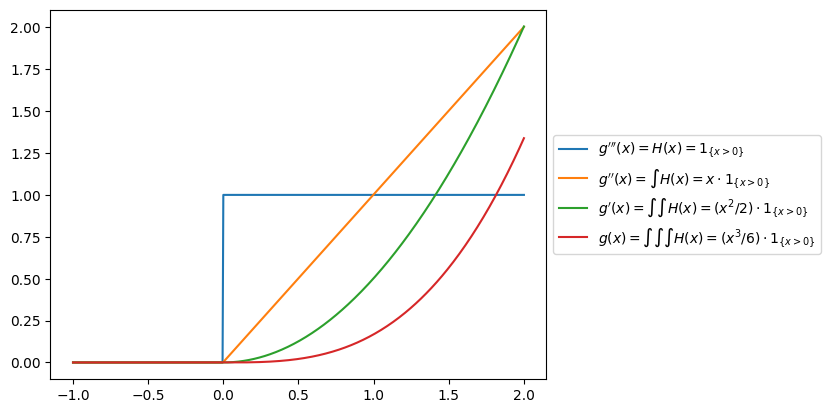

Piecewise Cubic Functions

The more times you integrate a piecewise function, the more smooth it becomes

We want \(f(0, T)\) to at least look like the green curve, no kinks, so \(TR(0, T)\) will look like the red curve, a piecewise cubic function

[36]:

from gfuncpy import gfunc, Identity

@gfunc

def H(x):

if x < 0:

return 0

else:

return 1

x = Identity([-1, 2])

gppp = H(x)

gpp = H(x).int()

gp = H(x).int().int()

g = H(x).int().int().int()

gppp.plot(label=r"$g'''(x) = H(x) = 1_{\{x>0\}}$")

gpp.plot(label=r"$g''(x) = \int H(x) = x\cdot 1_{\{x>0\}}$")

gp.plot(label=r"$g'(x) = \int\int H(x) = (x^2/2)\cdot 1_{\{x>0\}}$")

g.plot(label=r"$g(x) = \int\int\int H(x) = (x^3/6)\cdot 1_{\{x>0\}}$")

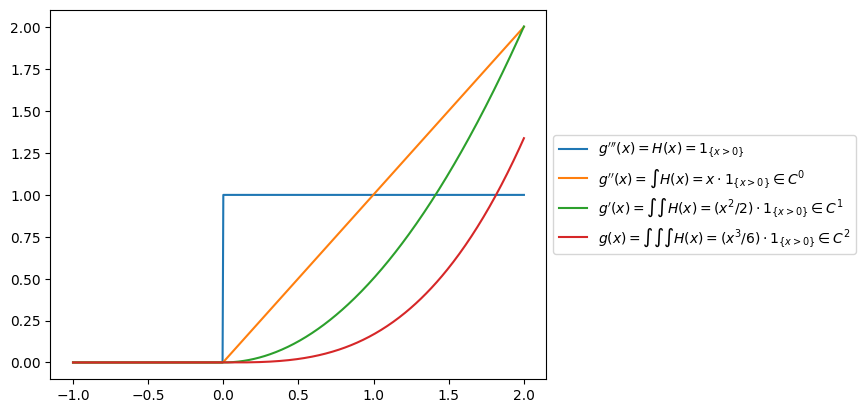

Function with Smoothness \(k\)

A function of class \(C^k\) is a function that has continuous derivatives up to the \(k\)-th order

\(f(x)\in C^2\) means all \(f(x)\), \(f'(x)\) and \(f''(x)\) are continuous but not \(f'''(x)\)

\(f(x)\in C^0\) means \(f(x)\) is continuous but not \(f'(x)\)

In fact, a \(C^0\) function must be non-differentiable at some point (at the kinks)

[37]:

from gfuncpy import gfunc, Identity

@gfunc

def H(x):

if x < 0:

return 0

else:

return 1

x = Identity([-1, 2])

gppp = H(x)

gpp = H(x).int()

gp = H(x).int().int()

g = H(x).int().int().int()

gppp.plot(label=r"$g'''(x) = H(x) = 1_{\{x>0\}}$")

gpp.plot(label=r"$g''(x) = \int H(x) = x\cdot 1_{\{x>0\}}\in C^0$")

gp.plot(label=r"$g'(x) = \int\int H(x) = (x^2/2)\cdot 1_{\{x>0\}}\in C^1$")

g.plot(label=r"$g(x) = \int\int\int H(x) = (x^3/6)\cdot 1_{\{x>0\}}\in C^2$")

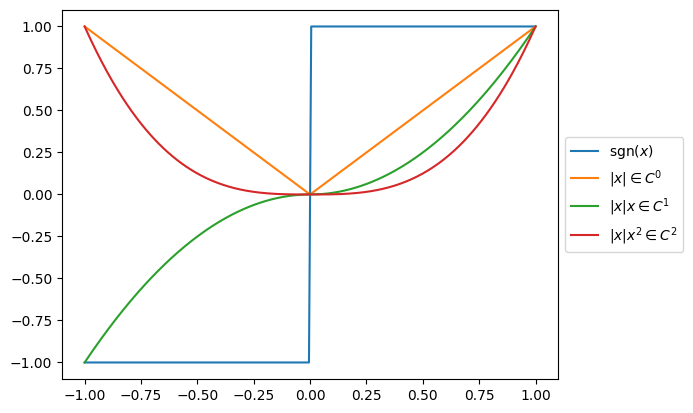

Another Way To Increase Smoothness

Multiplying a piecewise function \(f(x)\) with discontinuity \(c\) by a function \(g(x)\) that goes through 0 at \(c\) (meaning \(g(c)=0\)) removes the discontinuity

In the below example we have \(c=0\) and \(g(x) = x\)

The jump in the blue curve turns into a kink in the orange

[38]:

from gfuncpy import Identity, abs, sign

x = Identity([-1, 1])

sign(x).plot(label=r'$\text{sgn}(x)$')

abs(x).plot(label=r'$|x| \in C^0$')

(abs(x)*x).plot(label=r'$|x|x \in C^1$')

(abs(x)*(x**2)).plot(label=r'$|x|x^2 \in C^2$')

Interpolating Cubic Spline

An interpolating cubic spline \(s(x)\) is a piecewise function, a \(C^2\) function

The curve is a cubic function \(a_j x^3 + b_j x^2 + c_j x + d_j\) in each subinterval

Coefficients \(\{a_j\}, \{b_j\}, \{c_j\}, \{d_j\}\) are chosen to make \(s(x), s'(x), s''(x)\) continuous

Plot from SciPy documentation

Cubic Spline (Classic) Construction

One way to construct \(s(x)\) is to list equations for all coefficients and solve the system

If we have \(n\) subintervals, there will be \(4n\) coefficients

Each cubic polynomial has to go through the two end points in the corresponding subinterval, giving \(2n\) equations

Continuity of \(s'(x)\) at the knots (\(\{x_j\}_{j=0}^n\)) gives \(n-1\) equations

Continuity of \(s''(x)\) at the knots gives \(n-1\) equations

We are left with \(4n - 2n - (n-1) - (n-1) = 2\) degrees of freedom for boundary contitions

Natural boundary condition: \(s''(x_0) = s''(x_n) = 0\)

Cubic B-Spline Construction

A better way, known as the basis-spline, or the B-spline, is to construct \(s(x)\) as a linear combination of basis functions

\[s(x) = \sum_{j=0}^n c_j B_{j,3}(x)\]Basis functions can be precomputed and stored, speeding up the construction of \(s(x)\)

Easy to add/remove knots, it will be just reconstructing a few basis functions in the neighborhood that needs change

De Boor’s Algorithm

\[\begin{split}B_{i,0}(x) = \begin{cases} 1 & \text{if } \quad x_i \leq x < x_{i+1} \\ 0 & \text{otherwise} \end{cases}\end{split}\]\[B_{i,p}(x) = \frac{x - x_i}{x_{i+p} - x_i} B_{i,p-1}(x) + \frac{x_{i+p+1} - x}{x_{i+p+1} - x_{i+1}} B_{i+1,p-1}(x)\]

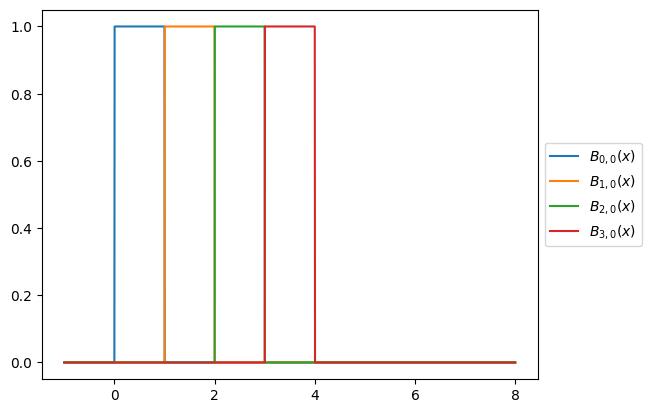

De Boor’s Algorithm: Piecewise Constant

Assuming \(x_j = j\), a uniform grid with grid spacing

\[\begin{split}B_{i,0}(x) = \begin{cases} 1 & \text{if } \quad x_i \leq x < x_{i+1} \\ 0 & \text{otherwise} \end{cases}\end{split}\]

[39]:

from functools import partial

from gfuncpy import gfunc

def B(x, idx):

if idx < x <= idx + 1:

return 1

else:

return 0

B_00 = gfunc(partial(B, idx=0))

B_10 = gfunc(partial(B, idx=1))

B_20 = gfunc(partial(B, idx=2))

B_30 = gfunc(partial(B, idx=3))

B_40 = gfunc(partial(B, idx=4))

B_50 = gfunc(partial(B, idx=5))

B_60 = gfunc(partial(B, idx=6))

x = Identity([-1, 8])

B_00(x).plot(label=r'$B_{0, 0}(x)$')

B_10(x).plot(label=r'$B_{1, 0}(x)$')

B_20(x).plot(label=r'$B_{2, 0}(x)$')

B_30(x).plot(label=r'$B_{3, 0}(x)$')

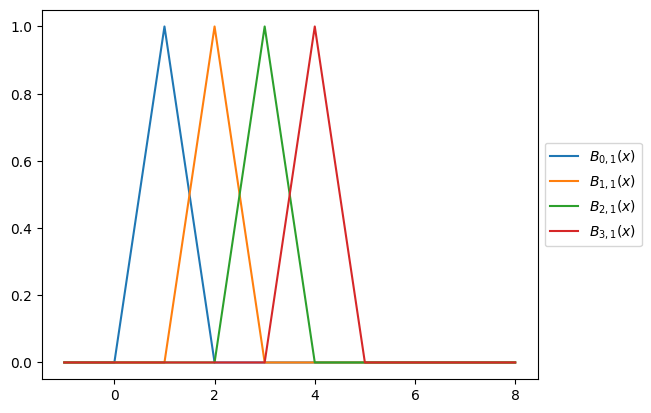

De Boor’s Algorithm: Piecewise Linear, \(C^0\)

Plug in \(x_j = j, p=1\): \begin{align*} B_{0,1}(x) &= (x-0) B_{0,0}(x) + (2-x) B_{1,0}(x)\qquad i=0, \\ B_{1,1}(x) &= (x-1) B_{1,0}(x) + (3-x) B_{2,0}(x)\qquad i=1, \\ B_{2,1}(x) &= (x-2) B_{2,0}(x) + (4-x) B_{3,0}(x)\qquad i=2, \\ B_{3,1}(x) &= (x-3) B_{3,0}(x) + (5-x) B_{4,0}(x)\qquad i=3\\ \end{align*}

De Boor’s Algorithm: Piecewise Linear, \(C^0\)

[40]:

B_01 = (x-0)*B_00(x) + (2-x)*B_10(x)

B_11 = (x-1)*B_10(x) + (3-x)*B_20(x)

B_21 = (x-2)*B_20(x) + (4-x)*B_30(x)

B_31 = (x-3)*B_30(x) + (5-x)*B_40(x)

B_41 = (x-4)*B_40(x) + (6-x)*B_50(x)

B_51 = (x-5)*B_50(x) + (7-x)*B_60(x)

B_01.plot(label=r'$B_{0, 1}(x)$')

B_11.plot(label=r'$B_{1, 1}(x)$')

B_21.plot(label=r'$B_{2, 1}(x)$')

B_31.plot(label=r'$B_{3, 1}(x)$')

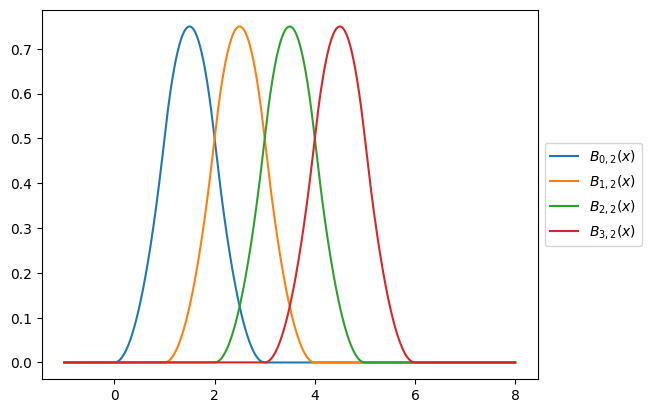

De Boor’s Algorithm: Piecewise Quadratic, \(C^1\)

Plug in \(x_j = j, p=2\): \begin{align*} B_{0,2}(x) &= \left(\frac{x-0}{2}\right) B_{0,1}(x) + \left(\frac{3-x}{2}\right) B_{1,1}(x)\qquad i=0, \\ B_{1,2}(x) &= \left(\frac{x-1}{2}\right) B_{1,1}(x) + \left(\frac{4-x}{2}\right) B_{2,1}(x)\qquad i=1, \\ B_{2,2}(x) &= \left(\frac{x-2}{2}\right) B_{2,1}(x) + \left(\frac{5-x}{2}\right) B_{3,1}(x)\qquad i=2, \\ B_{3,2}(x) &= \left(\frac{x-3}{2}\right) B_{3,1}(x) + \left(\frac{6-x}{2}\right) B_{4,1}(x)\qquad i=3\\ \end{align*}

De Boor’s Algorithm: Piecewise Quadratic, \(C^1\)

[41]:

B_02 = ((x-0)*B_01 + (3-x)*B_11)/2

B_12 = ((x-1)*B_11 + (4-x)*B_21)/2

B_22 = ((x-2)*B_21 + (5-x)*B_31)/2

B_32 = ((x-3)*B_31 + (6-x)*B_41)/2

B_42 = ((x-4)*B_41 + (7-x)*B_51)/2

B_02.plot(label=r'$B_{0, 2}(x)$')

B_12.plot(label=r'$B_{1, 2}(x)$')

B_22.plot(label=r'$B_{2, 2}(x)$')

B_32.plot(label=r'$B_{3, 2}(x)$')

De Boor’s Algorithm: Piecewise Cubic, \(C^2\)

Plug in \(x_j = j, p=3\): \begin{align*} B_{0,3}(x) &= \left(\frac{x-0}{3}\right) B_{0,2}(x) + \left(\frac{4-x}{3}\right) B_{1,2}(x)\qquad i=0, \\ B_{1,3}(x) &= \left(\frac{x-1}{3}\right) B_{1,2}(x) + \left(\frac{5-x}{3}\right) B_{2,2}(x)\qquad i=1, \\ B_{2,3}(x) &= \left(\frac{x-2}{3}\right) B_{2,2}(x) + \left(\frac{6-x}{3}\right) B_{3,2}(x)\qquad i=2, \\ B_{3,3}(x) &= \left(\frac{x-3}{3}\right) B_{3,2}(x) + \left(\frac{7-x}{3}\right) B_{4,2}(x)\qquad i=3\\ \end{align*}

De Boor’s Algorithm: Piecewise Cubic, \(C^2\)

[42]:

B_03 = ((x-0)*B_02 + (4-x)*B_12)/3

B_13 = ((x-1)*B_12 + (5-x)*B_22)/3

B_23 = ((x-2)*B_22 + (6-x)*B_32)/3

B_33 = ((x-3)*B_32 + (7-x)*B_42)/3

B_03.plot(label=r'$B_{0, 3}(x)$')

B_13.plot(label=r'$B_{1, 3}(x)$')

B_23.plot(label=r'$B_{2, 3}(x)$')

B_33.plot(label=r'$B_{3, 3}(x)$')

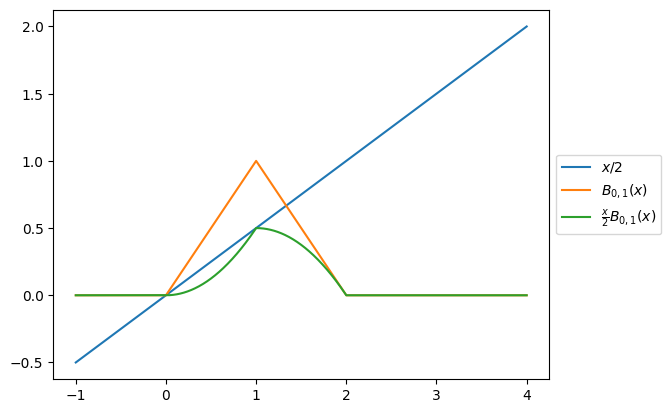

De Boor’s Algorithm: Why Does It Work?

From piecewise linear (\(C^0\)) to piecewise quadratic (\(C^1\))

\[B_{0,2}(x) = \underline{x B_{0,1}(x)/2} + (3-x) B_{1,1}(x)/2\]

[61]:

x = Identity([-1, 4])

B_01 = (x-0)*B_00(x) + (2-x)*B_10(x)

B_11 = (x-1)*B_10(x) + (3-x)*B_20(x)

(x/2).plot(label=r'$x/2$')

B_01.plot(label=r'$B_{0, 1}(x)$')

((x/2)*B_01).plot(label=r'$\frac{x}{2}B_{0, 1}(x)$')

De Boor’s Algorithm: Why Does It Work? (Cont.)

From piecewise linear (\(C^0\)) to piecewise quadratic (\(C^1\))

\[B_{0,2}(x) = \underline{x B_{0,1}(x)/2} + (3-x) B_{1,1}(x)/2\]

[62]:

((3-x)/2).plot(label=r'$x$')

B_11.plot(label=r'$B_{0, 1}(x)$')

(((3-x)/2)*B_11).plot(label=r'$(3-x)B_{1, 1}(x)$')

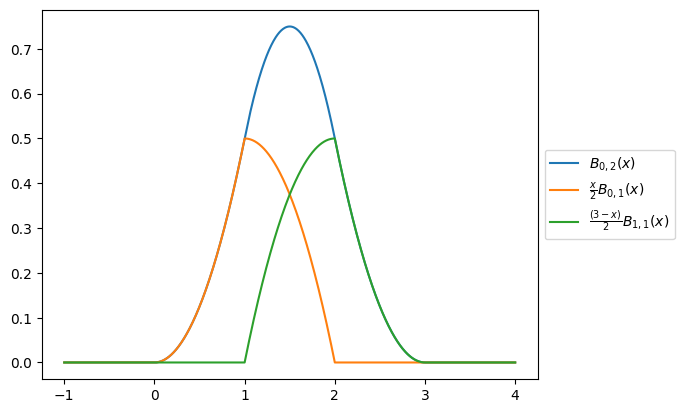

De Boor’s Algorithm: Why Does It Work? (Cont..)

From piecewise linear (\(C^0\)) to piecewise quadratic (\(C^1\))

\[B_{0,2}(x) = x B_{0,1}(x)/2~{\color{red}+}~(3-x) B_{1,1}(x)/2\]

[65]:

((x*B_01 + (3-x)*B_11)/2).plot(label=r'$B_{0, 2}(x)$')

(x*B_01/2).plot(label=r'$\frac{x}{2}B_{0, 1}(x)$')

((3-x)*B_11/2).plot(label=r'$\frac{(3-x)}{2}B_{1, 1}(x)$')

De Boor’s Algorithm: Non-Uniform Grid

The algorithm does not say anything about what the grid should be

In particular, the grid does not have to be uniform

In the market, liquid points on the curve (where we have reliable real time data) do not form a uniform grid

[ ]:

table('yc_long_end')

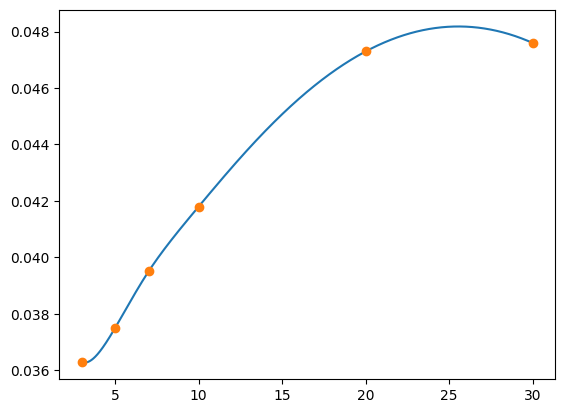

scipy.interpolate.CubicSpline Example

import numpy as np

from scipy.interpolate import CubicSpline

from gfuncpy import Identity, gfunc

import matplotlib.pyplot as plt

T_knots = np.array([3, 5, 7, 10, 20, 30])

R = np.array([3.63, 3.75, 3.95, 4.18, 4.73, 4.76])/100

cs = CubicSpline(T_knots, T_knots*R) # time weighted zero rate

@gfunc

def TR(x):

return cs(x)

T = Identity([3, 30])

(TR(T)/T).plot()

plt.plot(T_knots, R, 'o')

plt.show()

scipy.interpolate.CubicSpline Example (Cont.)

[81]:

import numpy as np

from scipy.interpolate import CubicSpline

from gfuncpy import Identity, gfunc

import matplotlib.pyplot as plt

T_knots = np.array([3, 5, 7, 10, 20, 30])

R = np.array([3.63, 3.75, 3.95, 4.18, 4.73, 4.76])/100

cs = CubicSpline(T_knots, T_knots*R) # time weighted zero rate

@gfunc

def TR(x):

return cs(x)

T = Identity([3, 30])

(TR(T)/T).plot()

plt.plot(T_knots, R, 'o')

plt.show()

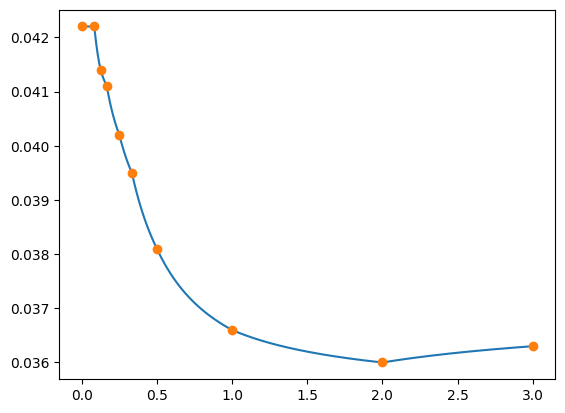

Front End of the Curve

import numpy as np

T_knots = np.array([1/365, 0.083333, 0.125, 0.16667, 0.25, 0.33333, 0.5, 1, 2, 3])

R = np.array([4.22, 4.22, 4.14, 4.11, 4.02, 3.95, 3.81, 3.66, 3.60, 3.63])/100

@gfunc

def TR(x):

return np.interp(x, T_knots, T_knots*R) # time weighted zero rate

T = Identity([0, 3])

(TR(T)/T).plot()

plt.plot(T_knots, R, 'o')

plt.show()

Front End of the Curve (Cont.)

In this toy example we assume the discontinuities are 1M, 1.5M, 2M, 3M, 4M, 6M, 1Y, 2Y and 3Y (it was supposed to be the FOMC meeting dates at the very short end)

Recall that without a quote, it’s flat extrapolation on the left

[87]:

import numpy as np

T_knots = np.array([0, 0.083333, 0.125, 0.16667, 0.25, 0.33333, 0.5, 1, 2, 3])

R = np.array([4.22, 4.22, 4.14, 4.11, 4.02, 3.95, 3.81, 3.66, 3.60, 3.63])/100

@gfunc

def TR(x):

return np.interp(x, T_knots, T_knots*R) # time weighted zero rate

T = Identity([0, 3])

(TR(T)/T).plot()

plt.plot(T_knots, R, 'o')

plt.show()

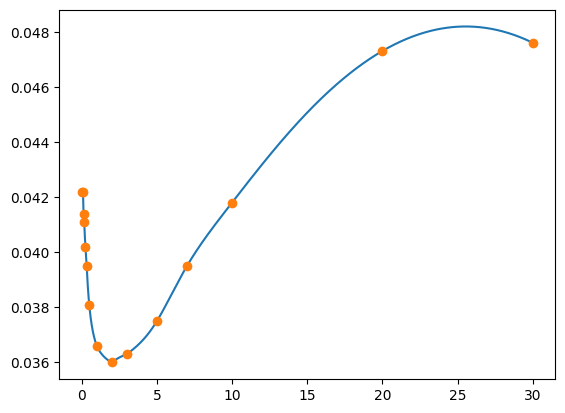

Entire Curve

import numpy as np

from scipy.interpolate import CubicSpline

from gfuncpy import Identity, gfunc

import matplotlib.pyplot as plt

T_knots = np.array([1/365, 0.083333, 0.125, 0.16667, 0.25, 0.33333, 0.5, 1, 2, 3, 5, 7, 10, 20, 30])

R = np.array([4.22, 4.22, 4.14, 4.11, 4.02, 3.95, 3.81, 3.66, 3.60, 3.63, 3.75, 3.95, 4.18, 4.73, 4.76])/100

cs = CubicSpline(T_knots, T_knots*R) # time weighted zero rate

@gfunc

def TR(x):

if x<3:

return np.interp(x, T_knots, T_knots*R)

else:

return cs(x)

T = Identity([0, 30])

(TR(T)/T).plot()

plt.plot(T_knots, R, 'o')

plt.show()

Entire Curve (Cont.)

[82]:

import numpy as np

from scipy.interpolate import CubicSpline

from gfuncpy import Identity, gfunc

import matplotlib.pyplot as plt

T_knots = np.array([1/365, 0.083333, 0.125, 0.16667, 0.25, 0.33333, 0.5, 1, 2, 3, 5, 7, 10, 20, 30])

R = np.array([4.22, 4.22, 4.14, 4.11, 4.02, 3.95, 3.81, 3.66, 3.60, 3.63, 3.75, 3.95, 4.18, 4.73, 4.76])/100

cs = CubicSpline(T_knots, T_knots*R) # time weighted zero rate

@gfunc

def TR(x):

if x<3:

return np.interp(x, T_knots, T_knots*R)

else:

return cs(x)

T = Identity([0, 30])

(TR(T)/T).plot()

plt.plot(T_knots, R, 'o')

plt.show()