12. SOFR Yield Curve Construction

[26]:

from fixedincome2025 import table

Overview

The SOFR yield curve is by far the most important curve if you work in a bank’s rates business

Most OTC products, e.g. swaps, use SOFR as the index rate

In this chapter, we study the SOFR yield curve construction

As we will see now, it is very different from Treasury yield curve construction

Curve Instruments

Unlike Treasury yield curve which is constructed from the Treasuries, there is no SOFR bonds

The SOFR yield curve is constructed from

Daily SOFR fixing for the day

3M SOFR futures

Standard SOFR swaps

3M SOFR futures and standard SOFR swaps are the most liquid rates instruments linked to the SOFR index

Curve Interpolation

Numerical settings same as explained in Curve Interpolation

Linear interpolation on the time weighted zero rate \(TR(0, T)\) at the short end

Cubic spline interpolated \(TR(0, T)\) for the rest of the curve

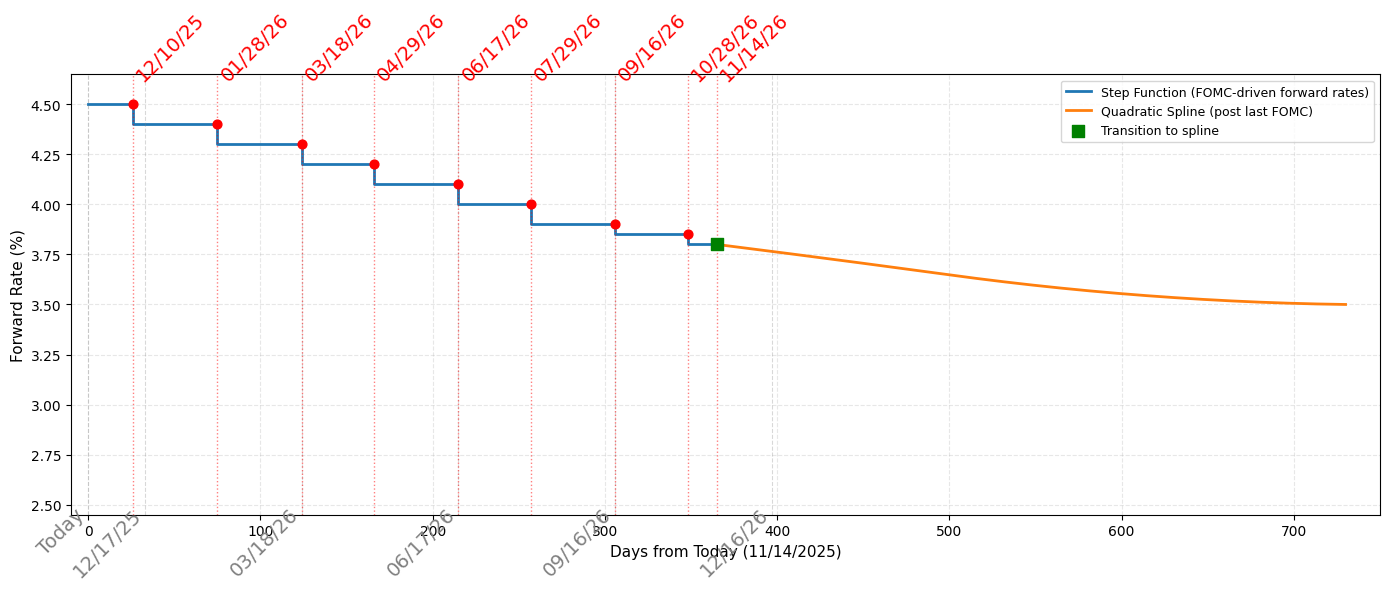

Which implies piecewise constant instantaneous forward rate \(f(0, T)\) at the short end and quadratic spline \(f(0, T)\) for the rest

Recall that

\[f(0, T) = \frac{d}{dT}[TR(0, T)]\]

Market Data

[69]:

table('curve_instruments')

[69]:

| Instrument | Quote | Convexity (bps) | |

|---|---|---|---|

| Deposit | 3.9700 | ||

| Futures Sep 25 | 95.9010 | 0 | |

| Futures Dec 25 | 96.1825 | 0.015563 | |

| Futures Mar 26 | 96.3925 | 0.091519 | |

| Futures Jun 26 | 96.6275 | 0.207215 | |

| Futures Sep 26 | 96.7875 | 0.362651 | |

| Swap 1y | 3.6151 | ||

| Swap 2y | 3.3980 | ||

| Swap 3y | 3.3624 | ||

| Swap 5y | 3.4232 | ||

| Swap 7y | 3.5379 | ||

| Swap 10y | 3.7120 | ||

| Swap 20y | 4.0420 | ||

| Swap 30y | 4.0199 |

Forward Rates

For each futures contract, the corresponding convexity adjustment is quoted, and we first compute forward rates by

\[\text{Forward Rate} = \text{Futures Rate} - \text{Convexity Adjustment}\]

[59]:

table('forward_rates')

[59]:

| Instrument | Quote (%) | |

|---|---|---|

| Futures Sep 25 | 4.100 | |

| Futures Dec 25 | 3.818 | |

| Futures Mar 26 | 3.608 | |

| Futures Jun 26 | ? | |

| Futures Sep 26 | ? |

Next we list the dates and compute year fractions

[51]:

table('key_dates')

[51]:

| Integer Year Fraction | IMM Dates | FOMC Meeting Dates | From Prev Key Date (Days) | From Today (Days) | Year Fraction | |

|---|---|---|---|---|---|---|

| 9/17/2025 | 9/17/2025 | 0 | -58 | -0.1589 | ||

| 10/29/2025 | 42 | -16 | -0.0438 | |||

| 11/14/2025 | 16 | 0 | 0.0000 | |||

| 12/10/2025 | 26 | 26 | 0.0712 | |||

| 12/17/2025 | 7 | 33 | 0.0904 | |||

| 1/28/2026 | 42 | 75 | 0.2055 | |||

| 3/18/2026 | 3/18/2026 | 49 | 124 | 0.3397 | ||

| 4/29/2026 | 42 | 166 | 0.4548 | |||

| 6/17/2026 | 6/17/2026 | 49 | 215 | 0.5890 | ||

| 7/29/2026 | 42 | 257 | 0.7041 | |||

| 9/16/2026 | 9/16/2026 | 49 | 306 | 0.8384 | ||

| 10/28/2026 | 42 | 348 | 0.9534 | |||

| 11/14/2026 | 17 | 365 | 1.0000 | |||

| 12/9/2026 | 25 | 390 | 1.0685 | |||

| 12/16/2026 | 7 | 397 | 1.0877 |

[80]:

import numpy as np

import datetime

df = table('key_dates').iloc[:, :3]

diff = np.diff(sorted([datetime.datetime.strptime(date_str, '%m/%d/%Y') for date_str in np.unique(df.values.flatten()) if date_str != ' ']))

yfs = [(td.days-58)/365 for td in diff.cumsum()]

yfs

[80]:

[-0.043835616438356165,

0.0,

0.07123287671232877,

0.09041095890410959,

0.2054794520547945,

0.33972602739726027,

0.4547945205479452,

0.589041095890411,

0.7041095890410959,

0.8383561643835616,

0.9534246575342465,

1.0,

1.0684931506849316,

1.0876712328767124]

[82]:

np.diff(yfs)

[82]:

array([0.04383562, 0.07123288, 0.01917808, 0.11506849, 0.13424658,

0.11506849, 0.13424658, 0.11506849, 0.13424658, 0.11506849,

0.04657534, 0.06849315, 0.01917808])

\(f(0, T)\) Implied From Futures Sep 2025

Recall that the instantaneous forward rate is a piecewise constant function with discontinuities being the FOMC meeting dates

In the period \([T, T+\tau]\) = [9/17/2025, 12/17/2025] there is a piecewise constant function with discontinuities at 10/29/2025 and 12/10/2025

We know the forward term rate for the reference quarter is \(4.1\%\)

With \(T=-0.1589\), \(T+\tau = 0.0904\), \(t=0\in [T, T+\tau]\), we have \begin{align*} 0.041 = L(t, T, T+\tau) &= \frac{1}{\tau}\left(\frac{P(t, T)}{P(t, T+\tau)} - 1\right) = \frac{1}{\tau}\left(\frac{M_t/M_T}{P(t, T+\tau)} - 1\right)\\ &= \frac{1}{\tau}\left(\frac{e^{\int_T^t r_u\,du }}{e^{-\int_t^{T+\tau} f(t, u)\,du}} - 1\right) = \frac{1}{\tau}\left(e^{\int_T^t r_u\,du + \int_t^{T+\tau} f(t, u)\,du} - 1\right)\\ \end{align*}

Current overnight rate is \(3.97\%\) and there was a rates cut of 25 bps at 10/29/2025, so \(r_s\) was fixed to be \(4.22\%\) before 10/29/2025 and \(3.97\%\) after

\(f(0, u)\) is \(3.97\%\) in the interval \(u\in\) [10/29/2025, 12/17/2025] and unknown after

For each date, find the corresponding year fraction

\(f(0, T)\) Implied From Futures Sep 2025 (Cont.)

We have \(\tau = (T+\tau) - T = 0.0904 + 0.1589 = 0.2493\) so \begin{align*} 0.041 &= L(0, T, T+\tau) \\ &= \frac{ e^{0.0422\times (-0.0438 -(-0.1589)) + 0.0397\times(0.0712 - (-0.0438)) + f_1\times(0.0904 - 0.0712))} - 1}{0.2493}, \end{align*} which solves to \(f_1 = 3.889\%\)

\(f(0, T)\) Implied From Futures Dec 2025

We have \(T=0.0904\), \(T+\tau = 0.3397\) so \(\tau = 0.2493\)

Forward rate for the reference quarter is \(3.818\%\)

In this reference quarter, there is only one meeting (one discountinuity), and we the first half of the \(f(0, u)\) function is \(3.889\%\), so \begin{align*} 0.03818 = L(t, T, T+\tau) &= \frac{1}{\tau}\left(e^{\int_T^{T+\tau} f(t, u)\,du} - 1\right)\\ &= \frac{e^{ 0.03889\times(0.2055 - 0.0904) + f_2\times(0.3397 - 0.2055)} - 1}{0.2493}, \end{align*} which solves to \(f_2 = 3.723563\%\)

\(f(0, T)\) Implied From Futures Mar 2026

We have \(T=0.3397\), \(T+\tau=0.5890\), so \(\tau=0.2493\) (again!)

Forward rate for the reference quarter is \(3.608\%\)

Both \(T\) and \(T+\tau\) are meeting dates and there is one more in the middle, so \begin{align*} 0.03608 = L(t, T, T+\tau) &= \frac{1}{\tau}\left(e^{\int_T^{T+\tau} f(t, u)\,du} - 1\right)\\ &= \frac{e^{ f_3\times(0.4548 - 0.3397) + f_4\times(0.5890 - 0.4548)} - 1}{0.2493} \end{align*}

Two variables with one equation, extra assumption has to be made

\(f(0, T)\) Implied From Futures Mar 2026 (Cont.)

\begin{align*} 0.03608 = \frac{e^{ f_3\times(0.4548 - 0.3397) + f_4\times(0.5890 - 0.4548)} - 1}{0.2493} \end{align*}

Two variables with one equation, extra assumption has to be made

By looking at the forward term rates, we know this part of the curve is still downward sloping: \(3.723563\% = f_2 > f_3 > f_4\)

The extra assumption is that the step sizes are the same: \(f_4 - f_3 = f_3 - f_2 = f_3 - 0.03723563\), which leads to \(f_4 = 2f_3 - 0.03723563\) and

\[0.03608 = \frac{e^{ f_3\times(0.4548 - 0.3397) + (2f_3 - 0.03723563)\times(0.5890 - 0.4548)} - 1}{0.2493},\]which solves to \(f_3 = 3.637954\%\) and \(f_4 = 2f_3 - 3.723563\% = 3.552345\%\)

Exercise: \(f(0, T)\) Implied From Futures Jun 2026 and Sep 2026

Like the previous reference quarter, we will have two variables with one equation for each futures

Using the same assumption

What’s \(f_5\) and \(f_6\) for futures Jun 2026?

What’s \(f_7\) and \(f_8\) for futures Sep 2026?

Swaps

We use the tenor structure \(T_j = j\) for the first few years

\(T_0 = 0\) is today 11/14/2025

\(T_1 = 1\) is 1 year from today

\(T_2 = 2\) is 2 years from today

\(\tau_n = T_{n+1} - T_n = 1\)

Recall that, we have the \(N\)-year spot starting swap rate formula \begin{align*} S(T_0) = \frac{1 - P(T_0, T_{N})}{A(T_0)},\qquad A(t) = \sum_{n=0}^{N-1}\tau_n P(t, T_{n+1}) \end{align*}

In particular, 1 year swap rate is

\[\frac{1 - P(T_0, T_1)}{\tau_0 P(T_0, T_1)} = \frac{1 - P(0, 1)}{P(0, 1)}\]

\(R(0, T_1)\) Implied From 1Y Swap

Given the 1y swap rate quote, we have \begin{align*} 0.036151 &= \frac{1 - P(0, 1)}{P(0, 1)}, \end{align*} which solves to

\[P(0, 1) = 0.96511029763\]and

\[R(0, 1) = -\log P(0, 1) = 3.551289\%\]Recall that \(R(0, T) = -(\log P(0, T))/T\)

\(f(0, T)\) Implied From 1Y Swap

But wait, it can also be written as \begin{align*} 0.036151 &= \frac{1 - P(0, 1)}{P(0, 1)}\\ &= \frac{1-e^{-\int_0^1 f(0, u)\,du}}{e^{-\int_0^1 f(0, u)\,du}}\\ \end{align*} which is in terms of \(f_1, f_2, \ldots, f_8\)

We should not have used extra assumption when computing \(f_7\) and \(f_8\). Instead, we should use one equation from futures and one from 1y swap to back them out

In general, whenever there is a quote, we don’t impose ad hoc assumptions

\(R(0, T_2)\) Implied From 2Y Swap

Given the 2y swap rate quote, we have \begin{align*} 0.03398 &= \frac{1 - P(0, 2)}{P(0, 1) + P(0, 2)}, \end{align*} but \(P(0, 1) = 0.96511\) is known, so \(P(0, 2)\) can be solved to be

\[P(0, 2) = 0.93542\]and

\[R(0, 2) = -(\log P(0, 2))/2 = 3.33798\%\]

The same process goes on and on until \(R(0, 30y)\) is found

We can then compute the entire curve by interpolating \(TR(0, T)\) at the knots

Exercise: \(R(0, T_3)\) Implied From 3Y Swap

Given the 3y swap rate quote \(3.3624\%\), find \(R(0, 3)\)

Bump and Revaluate and Delta Ladder

Today’s SOFR curve is the base scenario, and the portfolio value computed with today’s SOFR curve is the base PV (present value)

Base curve has the quotes: \(3.97\%, \$95.901, \$96.1825, \ldots, 3.6151\%, 3.398\%, \ldots\)

Bumped curves: Adding 1 bp to the rate at each bucket, we obtain 14 bumped curves (as there are 14 buckets on our SOFR curve)

The first one has quotes \(\underline{3.98\%}, \$95.901, \$96.1825, \ldots, 3.6151\%, 3.398\%, \ldots\)

The second one has quotes \(3.97\%, \underline{\$95.891}, \$96.1825, \ldots, 3.6151\%, 3.398\%, \ldots\)

The 7th one, corresponding to 1 bp bump on the 1y swap rate, has quotes \(3.97\%, \$95.901, \$96.1825, \ldots, \underline{3.6251\%}, 3.398\%, \ldots\)

Note that, in the futures buckets the quotes are prices, not rates, so the 1 bp bump should be subtracted from, not added to, the quotes

Revaluate the same portfolio with the 14 bumped curves to obtain 14 PVs

These 14 PVs minus the base PV give you 14 PV differences, which form the Delta ladder

[87]:

table('delta_ladder_sofr')

[87]:

| Delta | |

|---|---|

| Deposit | -185 |

| Futures Sep 25 | -231 |

| Futures Dec 25 | -303 |

| Futures Mar 26 | -275 |

| Futures Jun 26 | -690 |

| Futures Sep 26 | 778 |

| Swap 1y | -3739 |

| Swap 2y | -2320 |

| Swap 3y | 314 |

| Swap 5y | -65 |

| Swap 7y | 23 |

| Swap 10y | -6 |

| Swap 20y | 1 |

| Swap 30y | 0 |

| Sum | -6698 |

Closed Form Delta Ladder

Recall that, the Delta ladder of a ZCB (Treasury) on the Treasury yield curve has one single nonzero element, if the term of the ZCB happens to be a bucket

Similarly, a standard SOFR swap’s Delta ladder on the SOFR curve has one single nonzero element, if the term of the Swap happens to be a bucket

And the nonzero number is the swap’s PV change corresponding to 1 bp of the swap rate change, which is the swap’s PV01 \(A(T_0)\times 0.0001 \times N\), where \(N\) is the notional

[14]:

# SOFR Yield Curve Construction Timeline: Step Function → Quadratic Spline

import numpy as np

import matplotlib.pyplot as plt

from datetime import datetime

from scipy.interpolate import interp1d

# Define key dates

today = datetime(2025, 11, 14)

imm_dates = [

datetime(2025, 12, 17),

datetime(2026, 3, 18),

datetime(2026, 6, 17),

datetime(2026, 9, 16),

datetime(2026, 12, 16)

]

fomc_dates = [

datetime(2025, 12, 10),

datetime(2026, 1, 28),

datetime(2026, 3, 18),

datetime(2026, 4, 29),

datetime(2026, 6, 17),

datetime(2026, 7, 29),

datetime(2026, 9, 16),

datetime(2026, 10, 28),

datetime(2026, 11, 14)

]

# Convert to days from today for plotting

def to_days(dt):

return (dt - today).days

timeline_dates = [today] + imm_dates

timeline_days = [to_days(d) for d in timeline_dates]

fomc_days = [to_days(d) for d in fomc_dates]

# Create example step function values (hypothetical forward rates in %)

# Start at 4.5%, then step down at each FOMC meeting

step_values = [4.50, 4.40, 4.30, 4.20, 4.10, 4.00, 3.90, 3.85, 3.80]

# Build step function: piecewise constant between FOMC dates

x_step = []

y_step = []

for i, fomc_day in enumerate(fomc_days):

if i == 0:

# From today to first FOMC

x_step.extend([0, fomc_day])

y_step.extend([step_values[0], step_values[0]])

else:

# From previous FOMC to current FOMC

x_step.extend([fomc_days[i-1], fomc_day])

y_step.extend([step_values[i], step_values[i]])

# After last FOMC (11/14/2026), transition to quadratic spline

last_fomc_day = fomc_days[-1]

last_step_value = step_values[-1]

# Define a few points beyond last FOMC for quadratic spline (example: extending to 2 years out)

spline_days = [last_fomc_day, last_fomc_day + 90, last_fomc_day + 180, last_fomc_day + 365]

spline_values = [last_step_value, 3.70, 3.60, 3.50] # hypothetical declining rates

# Create quadratic spline interpolator

spline_func = interp1d(spline_days, spline_values, kind='quadratic', fill_value='extrapolate')

x_spline = np.linspace(last_fomc_day, spline_days[-1], 200)

y_spline = spline_func(x_spline)

# Plot

fig, ax = plt.subplots(figsize=(14, 6))

# Plot step function

ax.plot(x_step, y_step, color='#1f77b4', lw=2, label='Step Function (FOMC-driven forward rates)', drawstyle='steps-post')

# Plot quadratic spline

ax.plot(x_spline, y_spline, color='#ff7f0e', lw=2, label='Quadratic Spline (post last FOMC)')

# Mark today and IMM dates at the BOTTOM of the plot

for day, dt in zip(timeline_days, timeline_dates):

ax.axvline(day, color='gray', linestyle='--', alpha=0.3, lw=0.8)

# Place labels at bottom

label = 'Today' if dt == today else dt.strftime('%m/%d/%y')

ax.text(day, 2.50, label,

rotation=45, ha='right', va='top', fontsize=14, color='gray')

# Mark FOMC meeting dates at the TOP of the plot

for fomc_day, fomc_dt in zip(fomc_days, fomc_dates):

ax.axvline(fomc_day, color='red', linestyle=':', alpha=0.5, lw=1)

ax.scatter([fomc_day], [step_values[fomc_days.index(fomc_day)]],

color='red', s=40, zorder=5, marker='o')

# Place labels at top

ax.text(fomc_day, 4.60, fomc_dt.strftime('%m/%d/%y'),

rotation=45, ha='left', va='bottom', fontsize=14, color='red')

# Mark transition point (last FOMC)

ax.scatter([last_fomc_day], [last_step_value], color='green', s=80, zorder=6,

marker='s', label='Transition to spline')

# Formatting

ax.set_xlabel('Days from Today (11/14/2025)', fontsize=11)

ax.set_ylabel('Forward Rate (%)', fontsize=11)

# ax.set_title('SOFR Yield Curve Construction: FOMC Step Function → Quadratic Spline', fontsize=13, fontweight='bold')

ax.legend(loc='best', fontsize=9)

ax.grid(alpha=0.3, linestyle='--')

ax.set_xlim(-10, spline_days[-1] + 20)

ax.set_ylim(2.45, 4.65) # Adjust y-limits to accommodate labels at top and bottom

plt.tight_layout()

plt.show()