8. PCA

[4]:

from fixedincome2025 import table

Overview

So far we have covered

(Treasury) yield curve construction: A snap shot of the market

Duration and convexity: What happens to the portfolio value if the curve moves parallelly

Delta ladder: What happens to the portfolio value if the curve moves but not parallelly

Something is missing: How will tomorrow’s curve move?

Of course no one knows exactly, but we can still say something

Principal component analysis (PCA) provides a great tool to model yield curve movements and to hedge any portfolios that have rates exposure

Modeling Yield Curve Movements

Although the below curve has 14 points, when we model this curve’s movement, we should not model it by 14 independent random variables

[331]:

table('yc_10092025').T

[331]:

| 1m | 1.5m | 2m | 3m | 4m | 6m | 1y | 2y | 3y | 5y | 7y | 10y | 20y | 30y | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Yield | 4.2% | 4.17% | 4.11% | 4.03% | 3.95% | 3.83% | 3.66% | 3.6% | 3.59% | 3.74% | 3.92% | 4.14% | 4.7% | 4.72% |

Rates for nearby maturities on the curve tend to move together—both in direction and magnitude—because the corresponding bonds are close substitutes.

If 2y bond is too expensive, investors with the need can just buy 3y bond

If borrowing for 2y is too expensive, borrowers can just borrow for 3y

As we will see now, PCA tells us 3 independent random variables are enough

First we need some math

Singular Value Decomposition (SVD)

Every \(m\times n\) matrix \(X\) can be written as

\[X = USV^{\mathsf T},\]where

\(U\) is an \(m\times m\) unitary matrix (more on unitary matrices later)

\(V\) is an \(n\times n\) unitary matrix

\(S\) is an \(m\times n\) matrix with nonzero entries only on the main diagonal, meaning if \(S=(s_{ij})\), then \(s_{ij} \neq 0\) only when \(i = j\). Also the nonzero elements are sorted, meaning \(s_{11} \geq s_{22} \geq s_{33} \geq \cdots \geq s_{nn}\). They are known as the singular values of \(X\)

For our purpose which is to model the curve movement, the important case is \(m>n\)

The \(S\) Matrix

\(s_{11} \geq s_{22} \geq s_{33} \geq \cdots \geq s_{nn}\)

Unitary Matrix

Recall that \(X_{m\times n} = USV^{\mathsf T}\), where \(U_{m\times m}\) and \(V_{n\times n}\) are both unitary

Definition: A matrix \(V_{n\times n}\) is said to be unitary if \(V^{\mathsf T}V = I_n\), the \(n\times n\) identity matrix

Easy to compute inverse: \(V^{-1} = V^{\mathsf T}\) by definition

Let

\[\begin{split}V = \begin{pmatrix} |&|& & | \\ v_1 & v_2 & \cdots & v_n \\ |&|& & | \\ \end{pmatrix},\end{split}\]where \(v_j\) are column vectors

Unitary Matrix (Cont.)

\(V^{\mathsf T}V = I_n\): \begin{align*} V^{\mathsf T}V &= \begin{pmatrix} \frac{\qquad}{} & v_1^{\mathsf T} & \frac{\qquad}{} \\ \frac{\qquad}{} & v_2^{\mathsf T} & \frac{\qquad}{} \\ & \vdots & \\ \frac{\qquad}{} & v_n^{\mathsf T} & \frac{\qquad}{} \\ \end{pmatrix} \begin{pmatrix} |&|& & | \\ v_1 & v_2 & \cdots & v_n \\ |&|& & | \\ \end{pmatrix}\\ &= \begin{pmatrix} \langle v_1, v_1\rangle & \langle v_1, v_2\rangle & \cdots & \langle v_1, v_n\rangle\\ \langle v_2, v_1\rangle & \langle v_2, v_2\rangle & \cdots & \langle v_2, v_n\rangle\\ \vdots&\vdots&\ddots&\vdots \\ \langle v_n, v_1\rangle & \langle v_n, v_2\rangle & \cdots & \langle v_n, v_n\rangle \end{pmatrix} = \begin{pmatrix} 1 & 0 & \cdots & 0\\ 0 & 1 & \cdots & 0\\ \vdots&\vdots&\ddots&\vdots \\ 0 & 0 & \cdots & 1 \end{pmatrix}, \end{align*} where \(\langle \cdot, \cdot\rangle\) stands for the inner product of two vectors

Unitary means

The column vectors have norm 1 and

Inner product of any two different column vectors is 0

Vector Norm

Let \(\vec a = (a_1, a_2, \ldots, a_n)^{\mathsf T}\) be a column vector. Then its norm is \begin{align*} \lVert \vec a \rVert = \sqrt{\langle a, a\rangle} = \sqrt{a_1^2 + a_2^2 + \cdots + a_n^2} \end{align*}

Norm is the “length” of a vector in high dimensions

Inner Product

If \(\vec a = (a_1, a_2, \ldots, a_n)^{\mathsf T}\) and \(\vec b = (b_1, b_2, \ldots, b_n)^{\mathsf T}\), then \begin{align*} \langle \vec a, \vec b\rangle &= \vec a^{\mathsf T}\vec b = \vec b^{\mathsf T}\vec a \\ &= a_1b_1 + a_2b_2 + \cdots + a_nb_n \end{align*}

Zero Inner Product in 2D

Two vectors having zero inner product basically means they are “perpendicular”

Take 2D as an example. If \(v_1\) and \(v_2\) are in 2D and \(\langle v_1, v_2\rangle = 0\), write in polar coordinates \begin{align*} v_1 &= (r_1 \cos \theta_1, r_1 \sin \theta_1)^{\mathsf T}, \\ v_2 &= (r_2 \cos \theta_2, r_2 \sin \theta_2)^{\mathsf T}. \end{align*} Then \(\langle v_1, v_2\rangle = 0\) means \begin{align*} r_1 r_2 (\cos \theta_1 \cos \theta_2 + \sin \theta_1\sin \theta_2) = r_1 r_2 \cos (\theta_1 - \theta_2) = 0. \end{align*} So \(\theta_1 - \theta_2 = 90^{\circ}\) (plus multiples of \(180^{\circ}\)), so \(v_1\) and \(v_2\) are perpendicular.

In general, in 2D and 3D, inner product has the property

\[\langle \vec a, \vec b\rangle = \lVert \vec a \rVert\lVert \vec b \rVert \cos\theta,\]where \(\theta\) is the angle between the two vectors

Perpendicular in 2D

Perpendicular 2D vectors with norm 1 are just rotation of \((1, 0)^{\mathsf T}\) and \((0, 1)^{\mathsf T}\)

[332]:

import numpy as np

import matplotlib.pyplot as plt

# Example vectors in 2D

v1 = np.array([2.0, 1.0])

# perpendicular vector obtained by rotating v1 by 90 degrees: [-y, x]

v2 = np.array([-v1[1], v1[0]])

fig, ax = plt.subplots(figsize=(5,5))

# draw thin axes lines

ax.axhline(0, color='gray', linewidth=0.7)

ax.axvline(0, color='gray', linewidth=0.7)

# plot vectors using quiver so lengths are respected

ax.quiver(0, 0, v1[0], v1[1], angles='xy', scale_units='xy', scale=1, color='C0', width=0.02)

ax.quiver(0, 0, v2[0], v2[1], angles='xy', scale_units='xy', scale=1, color='C1', width=0.02)

# annotate tips

ax.annotate('v1', xy=(v1[0], v1[1]), xytext=(6,6), textcoords='offset points')

ax.annotate('v2', xy=(v2[0], v2[1]), xytext=(6,6), textcoords='offset points')

# determine symmetric plot limits and enforce equal aspect ratio

max_coord = np.max(np.abs(np.vstack((v1, v2)))) * 1.25

ax.set_xlim(-max_coord, max_coord)

ax.set_ylim(-max_coord, max_coord)

ax.set_aspect('equal', adjustable='box')

ax.set_xlabel('x')

ax.set_ylabel('y')

ax.set_title('Perpendicular 2D Vectors')

ax.grid(True, linestyle='--', linewidth=0.5)

plt.show()

Zero Inner Product in 3D

Similarly, in 3D, \(\langle v_1, v_2\rangle = \langle v_1, v_3\rangle = \langle v_2, v_3\rangle = 0\) means the 3 vectors are mutually perpendicular

This can be shown by first writing the vectors in spherical coordinates \begin{align*} \begin{cases} x = \sin \phi \cos \theta\\ y = \sin \phi \sin \theta\\ z = \cos \phi \end{cases}, \end{align*} but I’ll spare you the details

Perpendicular in 3D

Mutually perpendicular 3D vectors with norm 1 are just “rotation” of \((1, 0, 0)^{\mathsf T}\), \((0, 1, 0)^{\mathsf T}\) and \((0, 0, 1)^{\mathsf T}\)

[333]:

import numpy as np

import matplotlib.pyplot as plt

from mpl_toolkits.mplot3d import Axes3D

# Define three mutually perpendicular vectors in 3D

v1 = np.array([1.0, 1.0, 1.0])

v2 = np.array([1.0, -1.0, 0.0]) # v1.dot(v2) = 0

# v3 is chosen as the cross product v1 x v2 to ensure orthogonality and then scaled

v3 = np.cross(v1, v2)

v3 = v3 / np.linalg.norm(v3) * 1.5

fig = plt.figure(figsize=(6,6))

ax = fig.add_subplot(111, projection='3d')

# plot arrows from origin; arrow_length_ratio controls head size

ax.quiver(0, 0, 0, v1[0], v1[1], v1[2], color='C0', linewidth=1, arrow_length_ratio=0.08)

ax.quiver(0, 0, 0, v2[0], v2[1], v2[2], color='C1', linewidth=1, arrow_length_ratio=0.08)

ax.quiver(0, 0, 0, v3[0], v3[1], v3[2], color='C2', linewidth=1, arrow_length_ratio=0.08)

# annotate tips

ax.text(*(v1 * 1.05), 'v1', color='C0')

ax.text(*(v2 * 1.05), 'v2', color='C1')

ax.text(*(v3 * 1.05), 'v3', color='C2')

# symmetric limits around origin

max_coord = np.max(np.abs(np.vstack((v1, v2, v3)))) * 1.25

ax.set_xlim(-max_coord, max_coord)

ax.set_ylim(-max_coord, max_coord)

ax.set_zlim(-max_coord, max_coord)

# enforce equal aspect ratio if supported

try:

ax.set_box_aspect([1,1,1])

except Exception:

# older matplotlib: approximate equal aspect by leaving symmetric limits

pass

ax.set_xlabel('x')

ax.set_ylabel('y')

ax.set_zlabel('z')

# ax.set_title('Three Mutually Perpendicular 3D Vectors')

# Set a camera view (elevation, azimuth) to make perpendicular relationships easier to see

ax.view_init(elev=10, azim=20)

plt.show()

Zero Inner Product in General (\(n\)-D)

In 2D there can be at most 2 vectors that are mutually perpendicular

In 3D there can be at most 3 vectors that are mutually perpendicular

In general, in \(n\)-D there can be at most \(n\) vectors that are mutually perpendicular

In fact that’s the definition of the dimension in linear algebra: Maximum number of vectors one can find in a space that’s mutually independent

Given a set of mutually independent vectors, mutually perpendicular vectors can be constructed through the Gram-Schmidt process

An \(n\times n\) unitary matrix is one whose \(n\) column vectors are mutually perpendicular with norm 1

Such \(n\) vectors are just rotation of the so called standard basis \((1, 0,\ldots, 0)^{\mathsf T}\), \((0, 1,\ldots, 0)^{\mathsf T}\) and \((0, 0,\ldots, 1)^{\mathsf T}\)

Unitary Matrix as a Rotation Matrix

2D unit vector has the general form \((\cos\theta, \sin\theta)^{\mathsf T}\)

A 2D unit vector that’s perpendicular to \((\cos\theta, \sin\theta)^{\mathsf T}\) must be (?) \((\cos(\theta+\pi/2), \sin(\theta+\pi/2))^{\mathsf T} = (-\sin\theta, \cos\theta)^{\mathsf T}\)

The direction is unique but sign can change, that is, \(-(-\sin\theta, \cos\theta)^{\mathsf T}\) is also a perpendicular vector

Thus \(2\times 2\) unitary matrices have the general form \begin{align*} R = \begin{pmatrix} \cos\theta & -\sin\theta \\ \sin\theta & \cos\theta\\ \end{pmatrix}, \end{align*} which is a rotation matrix

\(R\) has a property that \(R\vec v\) rotates the direction of \(\vec v\) counterclockwise through \(\theta\)

In general, an \(n\times n\) unitary matrix is a rotation matrix that, when multiplied by an \(n\)-D vector, rotates the vector

One Property of SVD

Recall that \(X_{m\times n} = USV^{\mathsf T}\) with \(m>n\). We will write \(T = US\) and \(X = TV^{\mathsf T}\): \begin{align*} X_{m\times n} &= \begin{pmatrix} &\\ |&|& &&& | \\\\ u_1 & u_2 && \cdots && u_m \\\\ |&|& &&& | \\\\ \end{pmatrix}_{m\times m}\begin{pmatrix} s_{11} & 0 & \cdots & 0\\ 0 & s_{2, 1} & \cdots & 0\\ \vdots & \vdots & \ddots & \vdots\\ 0 & 0 & \cdots & s_{nn}\\ \vdots & \vdots & \vdots & \vdots\\ 0 & 0 & \cdots & 0\\ \end{pmatrix}_{m\times n}\begin{pmatrix} \frac{\qquad}{} & v_1^{\mathsf T} & \frac{\qquad}{} \\ \frac{\qquad}{} & v_2^{\mathsf T} & \frac{\qquad}{} \\ & \vdots & \\ \frac{\qquad}{} & v_n^{\mathsf T} & \frac{\qquad}{} \\ \end{pmatrix}_{n\times n}\\ &= TV^{\mathsf T} = \begin{pmatrix} \\ |&|& & | \\\\ s_{11} u_1 & s_{22} u_2 & \cdots & s_{nn}u_n \\\\ |&|& & | \\\\ \end{pmatrix}_{m\times n}\begin{pmatrix} \frac{\qquad}{} & v_1^{\mathsf T} & \frac{\qquad}{} \\ \frac{\qquad}{} & v_2^{\mathsf T} & \frac{\qquad}{} \\ & \vdots & \\ \frac{\qquad}{} & v_n^{\mathsf T} & \frac{\qquad}{} \\ \end{pmatrix}_{n\times n} \end{align*}

One Property of SVD (Cont.)

\begin{align*} X_{m\times n} = TV^{\mathsf T} = \begin{pmatrix} \\ |&|& & | \\\\ s_{11} u_1 & s_{22} u_2 & \cdots & s_{nn}u_n \\\\ |&|& & | \\\\ \end{pmatrix}_{m\times n}\begin{pmatrix} \frac{\qquad}{} & v_1^{\mathsf T} & \frac{\qquad}{} \\ \frac{\qquad}{} & v_2^{\mathsf T} & \frac{\qquad}{} \\ & \vdots & \\ \frac{\qquad}{} & v_n^{\mathsf T} & \frac{\qquad}{} \\ \end{pmatrix}_{n\times n} \end{align*}

\(T\), like \(U\), has mutually perpendicular column vectors too but with norms \(s_{11}, s_{22}, \ldots s_{nn}\)

For example \(\langle s_{11}u_1, s_{22}u_2\rangle = s_{11}s_{22}\langle u_1, u_2\rangle = 0\), as \(s_{11}\) and \(s_{22}\) are simply scalars

Numpy SVD Function

import numpy

u, s, vt = numpy.linalg.svd(X)

Curve PCA

We start from collecting the yield curve movement data

(curve on date \(t\)) - (curve on date \(t-1\))

If we use the Treasury yield curve for tenors \(\geq\) 1y, it has \(n=8\) points

We collect the daily curve movements from the past 3m (about \(m=66\) days)

The daily curve movement data forms the \(m\times n\) matrix \(X\), whose SVD gives \(X = TV^{\mathsf T}\)

Columns of \(V\), denoted by \(v_j\), are the principal components (PCs).

1st column \(v_1\) is PC1

2nd column \(v_2\) is PC2

3rd column \(v_3\) is PC3

Columns of \(T\) are PC scores

1st column is scores corresponding to PC1

2nd column is scores corresponding to PC2

3rd column is scores corresponding to PC3

Data

Curve data

[334]:

table('daily-treasury-rates').head(4).iloc[:, 6:]

[334]:

| 1y | 2y | 3y | 5y | 7y | 10y | 20y | 30y | |

|---|---|---|---|---|---|---|---|---|

| 10/17/2025 | 3.56 | 3.46 | 3.47 | 3.59 | 3.78 | 4.02 | 4.58 | 4.60 |

| 10/16/2025 | 3.54 | 3.41 | 3.42 | 3.55 | 3.74 | 3.99 | 4.56 | 4.58 |

| 10/15/2025 | 3.61 | 3.50 | 3.51 | 3.63 | 3.82 | 4.05 | 4.61 | 4.64 |

| 10/14/2025 | 3.58 | 3.48 | 3.47 | 3.60 | 3.79 | 4.03 | 4.59 | 4.62 |

Curve movement

[379]:

-table('daily-treasury-rates').head(4).iloc[:, 6:].diff()

[379]:

| 1y | 2y | 3y | 5y | 7y | 10y | 20y | 30y | |

|---|---|---|---|---|---|---|---|---|

| 10/17/2025 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 10/16/2025 | 0.02 | 0.05 | 0.05 | 0.04 | 0.04 | 0.03 | 0.02 | 0.02 |

| 10/15/2025 | -0.07 | -0.09 | -0.09 | -0.08 | -0.08 | -0.06 | -0.05 | -0.06 |

| 10/14/2025 | 0.03 | 0.02 | 0.04 | 0.03 | 0.03 | 0.02 | 0.02 | 0.02 |

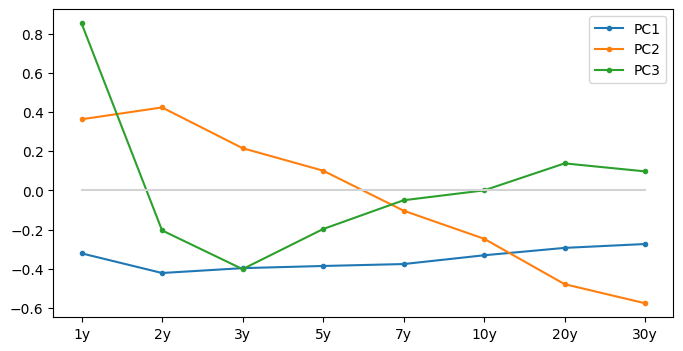

PCs

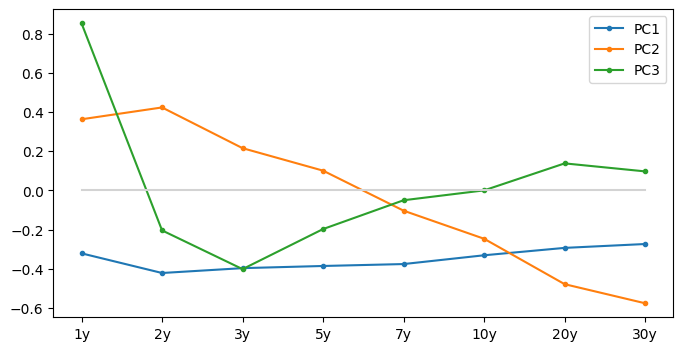

Classic result

PC1 is close to parallel shift

PC2 controls the slope of the curve

PC3 controls the curvature

[336]:

import numpy

X = -table('daily-treasury-rates').head(67).iloc[:, 6:].diff().dropna().values

m, n = X.shape

u, s, vt = numpy.linalg.svd(X)

T = u[:, :n] * s

v = vt.T

[337]:

from pandas import DataFrame

import matplotlib.pyplot as plt

import numpy as np

fig, ax = plt.subplots(figsize=(8, 4))

ax = DataFrame(v, columns=[f'PC{j}' for j in range(1, n+1)], index=['1y', '2y', '3y', '5y', '7y', '10y', '20y', '30y']).iloc[:, :3].plot(style='.-', ax=ax)

ax.plot(range(8), np.zeros(8), color='lightgray');

Scores

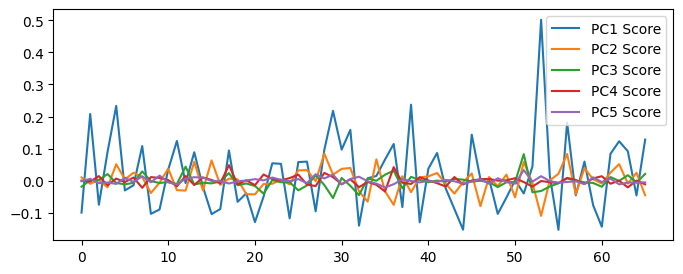

Classic result: PC1 score volatility \(\gg\) PC2 score volatility \(\gg\) PC3 score volatility

Given how tiny PC4 (and beyond) score volatility is, curve movements that can’t be explained by the first 3 PCs are often treated as noise

[338]:

(DataFrame(T, columns=[f'PC{j+1}' for j in range(n)])**2).mean().to_frame(name='Score Var').T

[338]:

| PC1 | PC2 | PC3 | PC4 | PC5 | PC6 | PC7 | PC8 | |

|---|---|---|---|---|---|---|---|---|

| Score Var | 0.014254 | 0.001473 | 0.000414 | 0.000197 | 0.000085 | 0.000035 | 0.000028 | 0.00002 |

[339]:

import matplotlib.pyplot as plt

fig, ax = plt.subplots(figsize=(8, 3))

DataFrame(T, columns=[f'PC{j} Score' for j in range(1, n+1)]).iloc[:, :5].plot(ax=ax);

What Just Happened? The Implication

Recall that \(X = TV^{\mathsf T}\). We have established that a unitary matrix like \(V\) is a rotation matrix, so \(X\) and \(T\) are the same data, simply rotated

Think of rows of \(X\) as independent sample points of the curve movement drawn from the same 8-dimensional distribution

Rows of \(T\) are then also independent sample points drawn from some 8-dimensional distribution

One row of \(X\) equals one row of \(T\) multiplied by \(V^{\mathsf T}\)

This is a conclusion from the block matrix multiplication

Block Matrix Multiplication

If all \(A, B, C, \ldots, H\) have the right sizes so that all the below operations are legal, then

\[\begin{split}\begin{pmatrix} \begin{array}{c|c} A & B\\ \hline C & D \end{array} \end{pmatrix} \begin{pmatrix} \begin{array}{c|c} E & F\\ \hline G & H \end{array} \end{pmatrix} = \begin{pmatrix} \begin{array}{c|c} AE+BG & AF+BH\\ \hline CE+DG & CF+DH \end{array} \end{pmatrix}\end{split}\]Legal means for example

Number of columns in \(A\) equals number of rows in \(E\) so that the matrix multiplication \(AE\) is defined

\(AE\) and \(BG\) have the the same size so that \(AE + BG\) is defined

That one row of \(X\) equals one row of \(T\) multiplied by \(V^{\mathsf T}\) if \(X = TV^{\mathsf T}\) is a special case where \(X\) and \(T\) are sliced into rows

The Implication (Cont.)

One row of \(X\) equals one row of \(T\) multiplied by \(V\) \begin{align*} \begin{pmatrix} x_{11} & x_{12} & \cdots & x_{1n} \end{pmatrix} &= \begin{pmatrix} t_{11} & t_{12} & \cdots & t_{1n} \end{pmatrix} V^{\mathsf T}\\ &= \begin{pmatrix} t_{11} & t_{12} & t_{13} & \cdots & t_{1n} \end{pmatrix} \begin{pmatrix} \frac{\qquad}{} & v_1^{\mathsf T} & \frac{\qquad}{}\\ \frac{\qquad}{} & v_2^{\mathsf T} & \frac{\qquad}{}\\ \frac{\qquad}{} & v_3^{\mathsf T} & \frac{\qquad}{}\\ &\vdots&\\ \end{pmatrix}\\ &= t_{11} \vec v_1^{\mathsf T} + t_{12} \vec v_2^{\mathsf T} + t_{13} \vec v_3^{\mathsf T} + t_{14} \vec v_4^{\mathsf T} + \cdots + t_{1n} \vec v_n^{\mathsf T}\\ &= t_{11} \vec v_1^{\mathsf T} + t_{12} \vec v_2^{\mathsf T} + t_{13} \vec v_3^{\mathsf T} + \vec\epsilon\\ \end{align*}

We obtain a 3-factor model for the yield curve movement \(\vec x\):

\[\vec x = t_1 \vec v_1 + t_2 \vec v_2 + t_3 \vec v_3 + \vec\epsilon,\]where \(t_1\), \(t_2\) and \(t_3\) are random variables, \(\vec\epsilon\) is a (small) random noise vector, and \(\vec v_1\), \(\vec v_2\) and \(\vec v_3\) are PCs from the data

Should We Center the Data?

Centering the data means find the average yield curve movement and subtract the average from the data

If we had centered the data with the average \(\vec x_{\text{avg}}\), we would have got \begin{align*} \vec x = \vec x_{\text{avg}} + t_{1} \vec v_1 + t_{2} \vec v_2 + t_{3} \vec v_3 + \vec\epsilon\\ \end{align*}

In practice, PCA is performed in a rolling period, and \(\vec x_{\text{avg}}\) would be a moving average

The 3-factor model is used to predict tomorrow’s yield curve movement. Whether to use the version with a moving average is personal choice

By not centering the data, we are saying \(E[\vec x] = \vec x_{\text{avg}} = \vec 0\)

One simple assumption that can lead to \(E[\vec x] = \vec 0\) is

\[E[t_1] = E[t_2] = E[t_3] = 0,\qquad E[\vec\epsilon] = \vec 0\]

Sample Covariance and Correlation

Recall that, if we have two random variables \(Y\), \(Z\), both with mean zero, and their samples \(\{Y_j\}_{j=1}^m\), \(\{Z_j\}_{j=1}^m\), the sample standard deviations and corvariance are \begin{align*} s_Y = \sqrt{\frac{\sum_{j=1}^m Y_j^2}{m-1}}, \qquad s_Z = \sqrt{\frac{\sum_{j=1}^m Z_j^2}{m-1}}, \qquad s_{YZ} = \frac{\sum_{j=1}^m Y_jZ_j}{m-1}, \end{align*} respectively, and the correlation is \(s_{YZ}/(s_Y s_Z)\)

When \(n\) goes to infinity, the sample standard deviations and corvariance converge to the theoretical value

\[\sqrt{E[Y^2]}, \qquad\sqrt{E[Z^2]}, \qquad E[YZ],\]respectively

If \(\sum_{j=1}^m Y_jZ_j = 0\), that will make the sample covariance and correlation both zero

If we treat the random realizations \(\{Y_j\}_{j=1}^m\) and \(\{Z_j\}_{j=1}^m\) as two \(m\)-dimensional vectors, zero inner product of these two vectors means the sample correlation is zero

3-Factor Model

The model:

\[\vec x = t_1 \vec v_1+ t_2 \vec v_2+ t_3 \vec v_3+ \vec\epsilon,\]where \(t_1\), \(t_2\) and \(t_3\) are random variables, \(\vec\epsilon\) is a (small) random noise vector, and \(\vec v_1\), \(\vec v_2\) and \(\vec v_3\) are PCs from the data

Now we know \(t_1\), \(t_2\) and \(t_3\) have zero sample correlations. A sensible assumption is that they are mutually independent

Be careful independence implies zero correlation, but the reverse is not true

We have also established the assumptions

\[E[t_1] = E[t_2] = E[t_3] = 0,\qquad E[\vec\epsilon] = \vec 0\]

The simplest concrete model is that \(t_1\), \(t_2\) and \(t_3\) are independently normally distributed with mean zero, and variances estimated by data

3-Factor Model Summary

Tomorrow’s yield curve movement is

\[\vec x = t_1 \vec v_1+ t_2 \vec v_2+ t_3 \vec v_3+ \vec\epsilon\]\(\vec\epsilon\) is a (small) random noise vector

\(\vec v_1\), \(\vec v_2\) and \(\vec v_3\) are PCs from the data

\(t_1\), \(t_2\) and \(t_3\) are independent normal random variables with mean 0, and their variances are estimated by data:

[340]:

(DataFrame(T, columns=[f'PC{j+1}' for j in range(n)])**2).mean().to_frame(name='Score Var').T

[340]:

| PC1 | PC2 | PC3 | PC4 | PC5 | PC6 | PC7 | PC8 | |

|---|---|---|---|---|---|---|---|---|

| Score Var | 0.014254 | 0.001473 | 0.000414 | 0.000197 | 0.000085 | 0.000035 | 0.000028 | 0.00002 |

PCs Revisited

PC1 is close to parallel shift

PC2 controls the slope of the curve

PC3 controls the curvature

[341]:

import numpy

X = -table('daily-treasury-rates').head(67).iloc[:, 6:].diff().dropna().values

m, n = X.shape

u, s, vt = numpy.linalg.svd(X)

T = u[:, :n] * s

v = vt.T

[342]:

from pandas import DataFrame

import matplotlib.pyplot as plt

import numpy as np

fig, ax = plt.subplots(figsize=(8, 4))

ax = DataFrame(v, columns=[f'PC{j}' for j in range(1, n+1)], index=['1y', '2y', '3y', '5y', '7y', '10y', '20y', '30y']).iloc[:, :3].plot(style='.-', ax=ax)

ax.plot(range(8), np.zeros(8), color='lightgray');

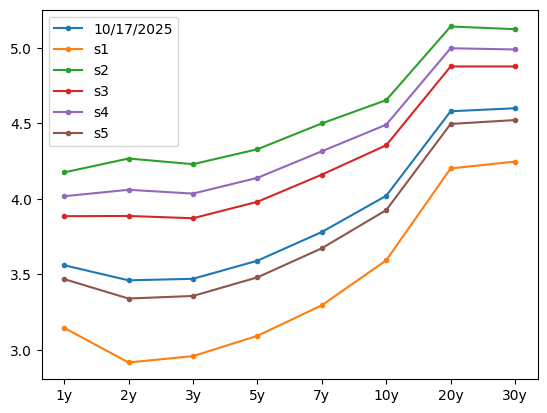

PC1 Scenarios: Parallel Shift

Holding \(t_2 = t_3 = 0\). A few possible realizations of \(t_1\) (std amplified 10 times for a better visualization, and same for PC2 and PC3 scenarios below)

[343]:

import numpy as np

n_scenarios = 5

# PCs

v1, v2, v3 = v[:, :3].T

# std of coefficients

std1, std2, std3 = 10*np.sqrt((DataFrame(T, columns=[f'PC{j+1}' for j in range(n)])**2).mean()).to_frame(name='Score Var').values.flatten()[:3]

# random scenarios

t1_scenarios = np.random.normal(loc=0, scale=std1, size=n_scenarios)

t2_scenarios = np.random.normal(loc=0, scale=std2, size=n_scenarios)

t3_scenarios = np.random.normal(loc=0, scale=std3, size=n_scenarios)

print(t1_scenarios)

[ 1.29061263 -1.91333395 -1.01081064 -1.42220717 0.28616997]

Scenario curves:

\[\text{Tomorrow's Curve $=$ Today's Curve $+\vec x + \vec\epsilon =$ Today's Curve $+t_1 \vec v_1 + \vec\epsilon$}\]

[344]:

import pandas as pd

curve_today = table('daily-treasury-rates').head(1).iloc[:, 6:].T

pc1_scenario_curves = pd.concat([curve_today, DataFrame(np.outer(v1, t1_scenarios) + curve_today.values, index=curve_today.index, columns=[f's{j}' for j in range(1, n_scenarios+1)])], axis='columns')

pc1_scenario_curves

[344]:

| 10/17/2025 | s1 | s2 | s3 | s4 | s5 | |

|---|---|---|---|---|---|---|

| 1y | 3.56 | 3.145144 | 4.175025 | 3.884916 | 4.017156 | 3.468013 |

| 2y | 3.46 | 2.915720 | 4.266895 | 3.886281 | 4.059776 | 3.339316 |

| 3y | 3.47 | 2.957706 | 4.229477 | 3.871230 | 4.034529 | 3.356408 |

| 5y | 3.59 | 3.091960 | 4.328345 | 3.980066 | 4.138822 | 3.479569 |

| 7y | 3.78 | 3.294604 | 4.499600 | 4.160163 | 4.314888 | 3.672372 |

| 10y | 4.02 | 3.592454 | 4.653837 | 4.354855 | 4.491140 | 3.925199 |

| 20y | 4.58 | 4.201118 | 5.141693 | 4.876741 | 4.997514 | 4.495990 |

| 30y | 4.60 | 4.246604 | 5.123910 | 4.876781 | 4.989430 | 4.521641 |

PC1 Scenarios: Parallel Shift (Cont.)

[345]:

pc1_scenario_curves.plot(style='.-');

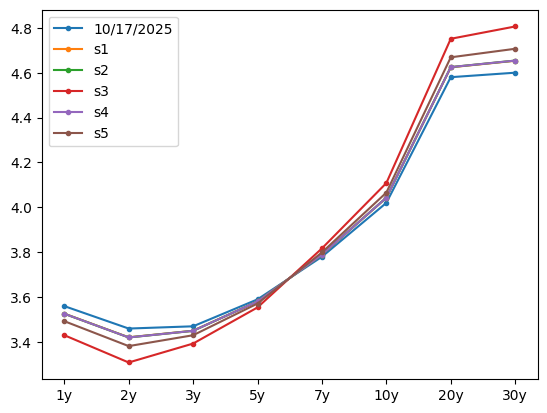

PC2 Scenarios: Slope Change

Holding \(t_1 = t_3 = 0\). A few possible realizations of \(t_2\):

[346]:

print(t2_scenarios)

[-0.09221954 -0.09366528 -0.35735591 -0.09354906 -0.18492912]

Scenario curves:

\[\text{Tomorrow's Curve $=$ Today's Curve $+t_2 \vec v_2 + \vec\epsilon$}\]

[347]:

pc2_scenario_curves = pd.concat([curve_today, DataFrame(np.outer(v2, t2_scenarios) + curve_today.values, index=curve_today.index, columns=[f's{j}' for j in range(1, n_scenarios+1)])], axis='columns')

pc2_scenario_curves

[347]:

| 10/17/2025 | s1 | s2 | s3 | s4 | s5 | |

|---|---|---|---|---|---|---|

| 1y | 3.56 | 3.526554 | 3.526030 | 3.430396 | 3.526072 | 3.492931 |

| 2y | 3.46 | 3.420985 | 3.420374 | 3.308816 | 3.420423 | 3.381763 |

| 3y | 3.47 | 3.450150 | 3.449839 | 3.393082 | 3.449864 | 3.430195 |

| 5y | 3.59 | 3.580736 | 3.580591 | 3.554101 | 3.580602 | 3.571423 |

| 7y | 3.78 | 3.789568 | 3.789718 | 3.817076 | 3.789706 | 3.799187 |

| 10y | 4.02 | 4.042783 | 4.043140 | 4.108285 | 4.043111 | 4.065687 |

| 20y | 4.58 | 4.624153 | 4.624845 | 4.751094 | 4.624789 | 4.668540 |

| 30y | 4.60 | 4.653139 | 4.653972 | 4.805918 | 4.653905 | 4.706561 |

PC2 Scenarios: Slope Change (Cont.)

Curve can “steepen” or “flatten”

[348]:

pc2_scenario_curves.plot(style='.-');

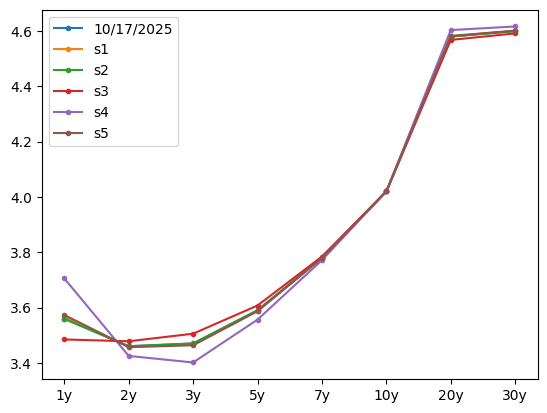

PC3 Scenarios: Curvature Change

Holding \(t_1 = t_2 = 0\). A few possible realizations of \(t_3\):

[349]:

print(t3_scenarios)

[ 0.00803162 -0.00072979 -0.08835312 0.17060337 0.01578796]

Scenario curves:

\[\text{Tomorrow's Curve $=$ Today's Curve $+t_3 \vec v_3 + \vec\epsilon$}\]

[350]:

pc3_scenario_curves = pd.concat([curve_today, DataFrame(np.outer(v3, t3_scenarios) + curve_today.values, index=curve_today.index, columns=[f's{j}' for j in range(1, n_scenarios+1)])], axis='columns')

pc3_scenario_curves

[350]:

| 10/17/2025 | s1 | s2 | s3 | s4 | s5 | |

|---|---|---|---|---|---|---|

| 1y | 3.56 | 3.566847 | 3.559378 | 3.484676 | 3.705446 | 3.573460 |

| 2y | 3.46 | 3.458359 | 3.460149 | 3.478053 | 3.425140 | 3.456774 |

| 3y | 3.47 | 3.466772 | 3.470293 | 3.505515 | 3.401424 | 3.463654 |

| 5y | 3.59 | 3.588414 | 3.590144 | 3.607448 | 3.556310 | 3.586882 |

| 7y | 3.78 | 3.779595 | 3.780037 | 3.784459 | 3.771391 | 3.779203 |

| 10y | 4.02 | 4.019999 | 4.020000 | 4.020007 | 4.019986 | 4.019999 |

| 20y | 4.58 | 4.581106 | 4.579900 | 4.567838 | 4.603483 | 4.582173 |

| 30y | 4.60 | 4.600777 | 4.599929 | 4.591452 | 4.616505 | 4.601527 |

PC3 Scenarios: Curvature Change (Cont.)

[351]:

pc3_scenario_curves.plot(style='.-');

Cumulative Percentage of Variance Explained

Recall the score matrix

\[\begin{split}T = \begin{pmatrix} t_{11} & t_{12} & \cdots & t_{1n}\\ t_{21} & t_{22} & \cdots & t_{2n}\\\\ &&\vdots& \\\\ t_{m1} & t_{m2} & \cdots & t_{mn} \end{pmatrix}_{m\times n}\end{split}\]We assume each column are realizations of a random variable with mean 0

Under the assumption, we find sample variance column by column. For example, the first column gives the variance \(\sum_{j=1}^m t_{j1}^2/m = 0.014254\), as listed below

[352]:

score_var = (DataFrame(T, columns=[f'PC{j+1}' for j in range(n)])**2).mean().to_frame(name='Score Var').T

score_var

[352]:

| PC1 | PC2 | PC3 | PC4 | PC5 | PC6 | PC7 | PC8 | |

|---|---|---|---|---|---|---|---|---|

| Score Var | 0.014254 | 0.001473 | 0.000414 | 0.000197 | 0.000085 | 0.000035 | 0.000028 | 0.00002 |

Cumulative Percentage of Variance Explained (Cont.)

Denote the variances by \(\text{Var}_1, \text{Var}_2, \ldots, \text{Var}_n\):

\[\text{Var}_k = \frac{1}{m}\sum_{j=1}^m t_{jk}^2\]The cumulative percentage of variance explained by the first \(k\) PCs are defined by

\[\frac{\text{Var}_1 + \text{Var}_2 + \cdots + \text{Var}_k}{\text{Var}_1 + \text{Var}_2 + \text{Var}_3 + \cdots + \text{Var}_n}\]Given the above data, the cumulative percentage of variance explained are

[353]:

var_explained = score_var.cumsum(axis='columns')/score_var.values.sum()

var_explained.index = ["Var Explained"]

var_explained

[353]:

| PC1 | PC2 | PC3 | PC4 | PC5 | PC6 | PC7 | PC8 | |

|---|---|---|---|---|---|---|---|---|

| Var Explained | 0.863574 | 0.952807 | 0.977915 | 0.989821 | 0.994952 | 0.997095 | 0.998814 | 1.0 |

PC1 alone explains 86% of the curve movement (the variances), PC1 and PC2 together explain 95%, and the first 3 PCs together explain almost 98%, which is quite common

Cumulative Percentage of Variance Explained (Cont..)

Recall the score matrix

\[\begin{split}T = US = \begin{pmatrix} t_{11} & t_{12} & \cdots & t_{1n}\\ t_{21} & t_{22} & \cdots & t_{2n}\\\\ &&\vdots& \\\\ t_{m1} & t_{m2} & \cdots & t_{mn} \end{pmatrix}_{m\times n} = \begin{pmatrix} \\ |&|& & | \\\\ s_{11} \vec u_1 & s_{22} \vec u_2 & \cdots & \vec s_{nn}u_n \\\\ |&|& & | \\\\ \end{pmatrix}_{m\times n}\end{split}\]and recall that \(\vec u_j\) has norm 1, so we have \begin{align*} \text{Var}_k = \frac{1}{m}\sum_{j=1}^m t_{jk}^2 = \frac{s_{kk}^2}{m} \sum_{j=1}^m u_{jk}^2 = \frac{s_{kk}^2}{m} \end{align*} and hence

\[\frac{\text{Var}_1 + \text{Var}_2 + \cdots + \text{Var}_k}{\text{Var}_1 + \text{Var}_2 + \text{Var}_3 + \cdots + \text{Var}_n} = \frac{s_{11}^2 + s_{22}^2 + \cdots + s_{kk}^2}{s_{11}^2 + s_{22}^2 + s_{33}^2 + \cdots + s_{nn}^2}\]

Cumulative Percentage of Variance Explained (Cont…)

u, s, vt = numpy.linalg.svd(X)

(s**2).cumsum()/(s**2).sum()

[360]:

# u, s, vt = numpy.linalg.svd(X)

print((s**2).cumsum()/(s**2).sum())

[0.86357429 0.95280679 0.97791528 0.9898212 0.994952 0.99709507

0.99881385 1. ]

Same as the previous table computed from the \(T\) matrix

[361]:

var_explained

[361]:

| PC1 | PC2 | PC3 | PC4 | PC5 | PC6 | PC7 | PC8 | |

|---|---|---|---|---|---|---|---|---|

| Var Explained | 0.863574 | 0.952807 | 0.977915 | 0.989821 | 0.994952 | 0.997095 | 0.998814 | 1.0 |

Applications in Hedging

Recall that, given the Delta ladder and the curve movement, we can compute the PnL of a portfolio

Having a model for tomorrow’s yield curve movement means having a model for tomorrow’s portfolio PnL

[5]:

delta_ladder = table('yc_10022025_10032025').iloc[-8:, 3].to_frame().T

delta_ladder

[5]:

| 1 Yr | 2 Yr | 3 Yr | 5 Yr | 7 Yr | 10 Yr | 20 Yr | 30 Yr | |

|---|---|---|---|---|---|---|---|---|

| Portfolio Delta Ladder | -3739 | -2320 | 314 | -65 | 23 | -6 | 1 | 0 |

Denote by \(\vec d\) the 8-dimensional Delta ladder

Recall that rows of \(X\) are the daily yield curve movement, treated as independent sample points:

[381]:

-table('daily-treasury-rates').head(4).iloc[:, 6:].diff().dropna()

[381]:

| 1y | 2y | 3y | 5y | 7y | 10y | 20y | 30y | |

|---|---|---|---|---|---|---|---|---|

| 10/16/2025 | 0.02 | 0.05 | 0.05 | 0.04 | 0.04 | 0.03 | 0.02 | 0.02 |

| 10/15/2025 | -0.07 | -0.09 | -0.09 | -0.08 | -0.08 | -0.06 | -0.05 | -0.06 |

| 10/14/2025 | 0.03 | 0.02 | 0.04 | 0.03 | 0.03 | 0.02 | 0.02 | 0.02 |

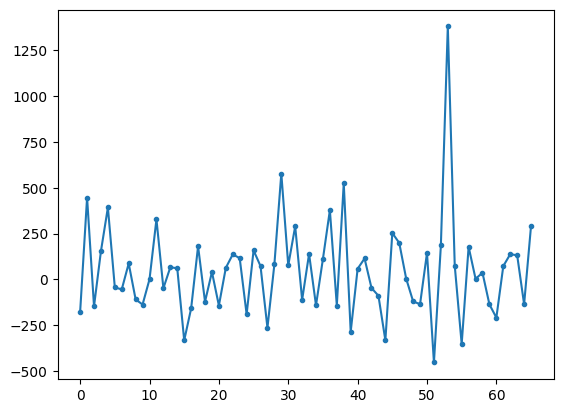

\(X\vec d\) is the daily PnL, a 66-dimensional vector

“If, on 10/16/2025, my portfolio Delta ladder is \(\vec d\), what’d have been the PnL?”

Daily PnL

[384]:

DataFrame(X @ d).plot(style='.-', legend=None);

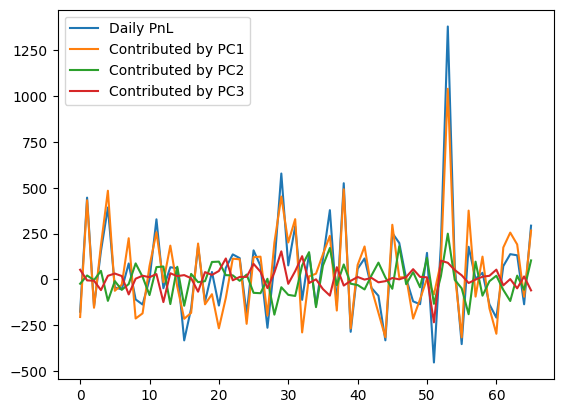

PnL Attribution

\begin{align*} X_{m\times n}\vec d &= TV^{\mathsf T} d \\ &= T_{m\times n}(V^{\mathsf T} d)_{n\times 1} \approx \langle v_1, \vec d\rangle \begin{pmatrix} t_{11} \\ t_{21} \\ \vdots \\ t_{m1} \end{pmatrix} + \langle v_2, \vec d\rangle \begin{pmatrix} t_{12} \\ t_{22} \\ \vdots \\ t_{m2} \end{pmatrix} + \langle v_3, \vec d\rangle \begin{pmatrix} t_{13} \\ t_{23} \\ \vdots \\ t_{m3} \end{pmatrix} \end{align*}

The 1st term is the daily PnL contributed by PC1 (parallel shift of the curve)

The 2nd term is the daily PnL contributed by PC2 (slope change of the curve)

The 3nd term is the daily PnL contributed by PC3 (curvature change of the curve)

PnL Attribution (Cont.)

[389]:

t1 = T.T[0]

t2 = T.T[1]

t3 = T.T[2]

DataFrame({'Daily PnL': X @ d,

'Contributed by PC1': (v1 @ d)*t1,

'Contributed by PC2': (v2 @ d)*t2,

'Contributed by PC3': (v3 @ d)*t3}).plot();

PnL Prediction

Tomorrow’s PnL is

\[\langle\vec x, \vec d\rangle \approx t_1\langle v_1, \vec d\rangle + t_2\langle v_2, \vec d\rangle + t_3\langle v_3, \vec d\rangle\]This is random as the coefficients \(t_1\), \(t_2\) and \(t_3\) are random

Recall that \(\text{Var}(t_1) \gg \text{Var}(t_2) \gg \text{Var}(t_3)\)

The 3 terms on the right hand side are PnL contributed by PC1, PC2 and PC3, respectively

As we have seen, PnL are mostly contributed by PC1 the parallel shift of the curve

This is a consequence of the fact that PC1 has by far the most volatile scores

Hedging out PC1 Risk

If we can hedge out PC1 risk, the portfolio will be much less volatile

We buy a 10y ZCB paying \(\$10,000\) at maturity, whose Delta ladder is as below

We choose 10y as the hedge instrument as it’s the most liquid

[10]:

from pandas import DataFrame

bond_10y_delta = DataFrame([[0, 0, 0, 0, 0, -6.6898, 0, 0]], columns=delta_ladder.columns, index=['Hedge Inst Delta'])

bond_2y_delta = DataFrame([[0, -1.86628, 0, 0, 0, 0, 0, 0]], columns=delta_ladder.columns, index=['Hedge Inst Delta'])

bond_10y_delta

[10]:

| 1 Yr | 2 Yr | 3 Yr | 5 Yr | 7 Yr | 10 Yr | 20 Yr | 30 Yr | |

|---|---|---|---|---|---|---|---|---|

| Hedge Inst Delta | 0 | 0 | 0 | 0 | 0 | -6.6898 | 0 | 0 |

Denote this Delta ladder of the hedge instruemnt as \(\vec b_1\)

Hedge Ratio

Adding \(h\) units of the hedge instrument into the portfolio, the portfolio Delta ladder becomes \(\vec d + h \vec b_1\) and tomorrow’s PnL becomes

\[\langle\vec x, \vec d + h \vec b_1\rangle \approx t_1\langle v_1, \vec d + h \vec b_1\rangle + t_2\langle v_2, \vec d + h \vec b_1\rangle + t_3\langle v_3, \vec d + h \vec b_1\rangle\]If we want to hedge out PC1 risk, we must have \(\langle v_1, \vec d + h \vec b_1\rangle = 0\)

If this term is zero, the PnL can only come from less volatile \(t_2\) and \(t_3\)

We have

\[0 = \langle v_1, \vec d + h \vec b_1\rangle = \langle v_1, \vec d\rangle + h \langle v_1, \vec b_1\rangle,\]or

\[h = -\frac{\langle v_1, \vec d\rangle}{\langle v_1, \vec b_1\rangle}\]This is the hedge ratio. This is how much of the hedge instrument we must add to the portfolio to make it immue to curve parallel shift

Hedge Ratio: Exercise

Given the portfolio Delta ladder

[401]:

delta_ladder

[401]:

| 1 Yr | 2 Yr | 3 Yr | 5 Yr | 7 Yr | 10 Yr | 20 Yr | 30 Yr | |

|---|---|---|---|---|---|---|---|---|

| Portfolio Delta Ladder | -3739 | -2320 | 314 | -65 | 23 | -6 | 1 | 0 |

And the Delta ladder of a 10y ZCB paying \(\$10,000\) at maturity

[11]:

bond_10y_delta

[11]:

| 1 Yr | 2 Yr | 3 Yr | 5 Yr | 7 Yr | 10 Yr | 20 Yr | 30 Yr | |

|---|---|---|---|---|---|---|---|---|

| Hedge Inst Delta | 0 | 0 | 0 | 0 | 0 | -6.6898 | 0 | 0 |

And the PC1 vector

[411]:

print(v1)

[-0.32144131 -0.42172197 -0.39693884 -0.3858943 -0.37609721 -0.33127384

-0.29356772 -0.27382061]

Please compute the hedge ratio

Hedging out Both PC1 and PC2 Risk

One can hedge out both PC1 and PC2 risk to make the portfolio immune to both parallel shift and slope change of the curve

We buy \(h_1\) units of 10y ZCB paying \(\$10,000\) at maturity, whose Delta ladder, denoted by \(\vec b_1\), is as below

[12]:

bond_10y_delta

[12]:

| 1 Yr | 2 Yr | 3 Yr | 5 Yr | 7 Yr | 10 Yr | 20 Yr | 30 Yr | |

|---|---|---|---|---|---|---|---|---|

| Hedge Inst Delta | 0 | 0 | 0 | 0 | 0 | -6.6898 | 0 | 0 |

We further buy \(h_2\) units of 2y ZCB paying \(\$10,000\) at maturity, whose Delta ladder, denoted by \(\vec b_2\), is as below

[13]:

bond_2y_delta

[13]:

| 1 Yr | 2 Yr | 3 Yr | 5 Yr | 7 Yr | 10 Yr | 20 Yr | 30 Yr | |

|---|---|---|---|---|---|---|---|---|

| Hedge Inst Delta | 0 | -1.86628 | 0 | 0 | 0 | 0 | 0 | 0 |

Hedging out Both PC1 and PC2 Risk (Cont.)

The hedged portfolio Delta ladder is \(\vec d + h_1 \vec b_1 + h_2 \vec b_2\) and tomorrow’s PnL becomes \begin{align*} &\langle\vec x, \vec d + h_1 \vec b_1 + h_2 \vec b_2\rangle \\ &\approx t_1\langle v_1, \vec d + h_1 \vec b_1 + h_2 \vec b_2\rangle + t_2\langle v_2, \vec d + h_1 \vec b_1 + h_2 \vec b_2\rangle + t_3\langle v_3, \vec d + h_1 \vec b_1 + h_2 \vec b_2\rangle \end{align*}

In order to hedge out both PC1 and PC2 risk, we must have \begin{align*} 0 &= \langle v_1, \vec d + h_1 \vec b_1 + h_2 \vec b_2\rangle = \langle v_1, \vec d\rangle + h_1 \langle v_1, \vec b_1\rangle + h_2 \langle v_1, \vec b_2\rangle,\\ 0 &= \langle v_2, \vec d + h_1 \vec b_1 + h_2 \vec b_2\rangle = \langle v_2, \vec d\rangle + h_1 \langle v_2, \vec b_1\rangle + h_2 \langle v_2, \vec b_2\rangle \end{align*}

If these two terms are both zero, tomorrow’s PnL can only come from much less volatile \(t_3\)

This linear system can be solved to obtain the hedge ratios, that’s units of 10y and 2y ZCB we need to buy to make the portfolio immune to both parallel shift and slope change of the curve