14. Volatility and IR Options

Overview

The most liquid nonlinear OCT rates products are SOFR caps, floors and SOFR swaptions

This chapter is an overview of SOFR caps, floors and swaptions, and their pricing and heding

Sell Side Rates Options Business

In the rates options business, there are exotic products and vanilla products

Vanilla products: SOFR caps, floors and SOFR swaptions

Examples of exotics: Bermudan swaptions, CMS swaps, CMS caps and floors, CMS spread options, range accrual

Exotic desk traders hedge their books by trading vanilla products

Vanilla desk traders do so by trading underlying linear products (SOFR swaps, FRA or futures)

More complicated models are needed for exotics pricing and hedging

Since exotics are hedged by vanillas, the pricing model has to give consistent pricing of both exotics and vanillas

Thus, the models are calibrated to vanillas

Sell Side Rates Options Business (Cont.)

All risk hedged out, where is the revenue from?

Think of zero delta ladder, portfolio PnL will be zero no matter how the market moves

Traders can still intentionally over/under hedge, taking directional risk, but there is in house delta limit as regulator is watching

Part of the revenue is from fees and bid ask spreads

The more exotic the product is, the higher the fees and bid ask spreads, and hence the revenue

Justified by the significant investment in a quant team of PhDs to build and maintain the model, the hardware, and limited market players

Only 4-5 banks have a working model to quote/trade all rates exotics

Even with a working model, sometimes trade from a client can be too risky for small banks to take in

The larger the book is, the more risk a bank can safely take

Option Pricing Basics

PV of an option can be computed by no-arbitrage argument, like many previous examples

But unlike previous no-arbitrage arguments, option pricing requires assumptions (models)

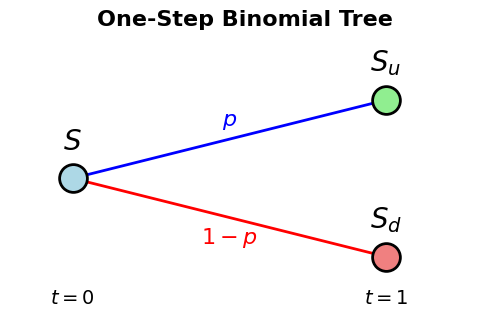

The simpliest option pricing model is the Binomial Option Pricing Model (BOPM)

BOPM Assumptions

We want to price an option on a stock trading at \(S\) currently

There are only two discrete times (one time step)

Today at \(t=0\),

Maturity of the option at \(t=1\)

At \(t=1\), the stock price can either go up to \(S_u\) or go down to \(S_d\) (two states)

Option payoff at \(t=1\) is \(C_u\) if the stock goes up and \(C_d\) if it goes down

If it is a call option then \(C_u = (S_u - K)^+\) and \(C_d = (S_d - K)^+\)

[20]:

# Single-step binomial tree visualization

import matplotlib.pyplot as plt

import matplotlib.patches as mpatches

fig, ax = plt.subplots(figsize=(5, 3))

# Node positions

t0_x, t0_y = 0, 0.5

t1_u_x, t1_u_y = 1, 0.75

t1_d_x, t1_d_y = 1, 0.25

# Draw edges (branches)

ax.plot([t0_x, t1_u_x], [t0_y, t1_u_y], 'b-', lw=2, label='Up move')

ax.plot([t0_x, t1_d_x], [t0_y, t1_d_y], 'r-', lw=2, label='Down move')

# Draw nodes

node_size = 400

ax.scatter([t0_x], [t0_y], s=node_size, c='lightblue', edgecolors='black', zorder=5, linewidths=2)

ax.scatter([t1_u_x], [t1_u_y], s=node_size, c='lightgreen', edgecolors='black', zorder=5, linewidths=2)

ax.scatter([t1_d_x], [t1_d_y], s=node_size, c='lightcoral', edgecolors='black', zorder=5, linewidths=2)

# Add labels

ax.text(t0_x, t0_y+0.12, r'$S$', fontsize=20, ha='center', va='center', fontweight='bold')

ax.text(t1_u_x, t1_u_y+0.12, r'$S_u$', fontsize=20, ha='center', va='center', fontweight='bold')

ax.text(t1_d_x, t1_d_y+0.12, r'$S_d$', fontsize=20, ha='center', va='center', fontweight='bold')

# Add probability labels on branches

ax.text(0.5, 0.65, r'$p$', fontsize=16, ha='center', va='bottom', color='blue', style='italic')

ax.text(0.5, 0.35, r'$1-p$', fontsize=16, ha='center', va='top', color='red', style='italic')

# Time labels

ax.text(t0_x, 0.15, r'$t=0$', fontsize=14, ha='center', va='top')

ax.text(t1_u_x, 0.15, r'$t=1$', fontsize=14, ha='center', va='top')

# Formatting

ax.set_xlim(-0.2, 1.3)

ax.set_ylim(0.2, 0.9)

ax.set_aspect('equal')

ax.axis('off')

ax.set_title('One-Step Binomial Tree', fontsize=16, fontweight='bold', pad=20)

plt.tight_layout()

plt.show()

BOPM No-Arbitrage Argument

We set up a portfolio so that, at \(t=1\), the portfolio value replicates the option in both states

By no-arbitrage argument, the option price at \(t=0\) should equals the portfolio value at \(t=0\)

The portfolio setup at \(t=0\):

Buy \(h\) share of the stock at \(S\)

Deposit \(B\) dollars into the money market account (MMA)

Initial portfolio value is \(hS+B\)

At \(t=1\) there are two states

Stock position value goes up to \(hS_u\) and cash in MMA grows into \(BM\) dollars

Stock position value goes down to \(hS_d\) and cash in MMA grows into \(BM\) dollars

To replicate the option payoff, set \begin{align*} hS_u + BM &= C_u\\ hS_d + BM &= C_d \end{align*}

Solve for \(h\) and \(B\) and find the initial portfolio value, which should equal the option price

BOPM

We have the system of equations written in matrix form \begin{align*} \begin{pmatrix} S_u & M\\ S_d & M \end{pmatrix} \begin{pmatrix} h \\ B \end{pmatrix} = \begin{pmatrix} C_u \\ C_d \end{pmatrix} \end{align*}

The solution is \begin{align*} \begin{pmatrix} h \\ B \end{pmatrix} = \frac{1}{M(S_u - S_d)} \begin{pmatrix} M & -M\\ -S_d & S_u \end{pmatrix} \begin{pmatrix} C_u \\ C_d \end{pmatrix} \end{align*}

The option price is \(hS + B\), or \begin{align*} \begin{pmatrix} S & 1 \end{pmatrix} \begin{pmatrix} h \\ B \end{pmatrix} &= \frac{1}{M(S_u - S_d)} \begin{pmatrix} S & 1 \end{pmatrix} \begin{pmatrix} M & -M\\ -S_d & S_u \end{pmatrix} \begin{pmatrix} C_u \\ C_d \end{pmatrix}\\ &= \frac{1}{M} \begin{pmatrix} \frac{SM - S_d}{S_u - S_d} & \frac{S_u - SM}{S_u - S_d} \end{pmatrix} \begin{pmatrix} C_u \\ C_d \end{pmatrix}\\ &= \frac{1}{M} \left( \frac{SM - S_d}{S_u - S_d} C_u + \frac{S_u - SM}{S_u - S_d} C_d \right) \end{align*}

BOPM Discussion

PV of the option at \(t=0\):

\[C = \frac{1}{M} \left( \frac{SM - S_d}{S_u - S_d} C_u + \frac{S_u - SM}{S_u - S_d} C_d \right),\]where \(1/M\) is the discount factor and

\[\frac{SM - S_d}{S_u - S_d} + \frac{S_u - SM}{S_u - S_d} = 1,\]which allows us to see \(C\) as a discounted expectation of possible option payoff

Weighted average with weights sum to 1 is an expectation

We write

\[\tilde p = \frac{SM - S_d}{S_u - S_d}, \qquad (1-\tilde p) = \frac{S_u - SM}{S_u - S_d},\]known as the risk neutral probability, different from the physical probability \((p, 1-p)\)

The precise statement is, \(C\) is a discounted expectation of possible option payoff under the risk neutral probability

BOPM Discussion (Cont.)

The physical probability \((p, 1-p)\) doesn’t go into option pricing

No matter how large \(p\) is (how likely the stock price will go up), the call option price doesn’t go up a bit in BOPM

Remember the option price we obtained is by a no-arbitrage argument. Quoting a different price will lead to an arbitrage opportunity

BOPM: Example

Consider an ATM call option in BOPM with \(S = K = 100\), \(K\) the strike price, and \(S_u = 105\), \(S_d = 95\), \(M=1.01\). Option payoff at \(t=1\) is \begin{align*} C_u &= (S_u - K)^+ = 5\\ C_d &= (S_d - K)^+ = 0 \end{align*}

PV of the option at \(t=0\) is \begin{align*} C &= \frac{1}{M} \left( \frac{SM - S_d}{S_u - S_d} C_u + \frac{S_u - SM}{S_u - S_d} C_d \right)\\ &= \frac{1}{1.01}\left( \frac{101 - 95}{105 - 95} \times 5 + \frac{105 - 101}{105 - 95} \times 0 \right) = \$ 2.970297 \end{align*}

BOPM: Example (Cont.)

One can compute the replicating portfolio as follows \begin{align*} \begin{pmatrix} h \\ B \end{pmatrix} &= \frac{1}{M(S_u - S_d)} \begin{pmatrix} M & -M\\ -S_d & S_u \end{pmatrix} \begin{pmatrix} C_u \\ C_d \end{pmatrix}\\ &= \frac{1}{1.01\times (105 - 95)} \begin{pmatrix} 1.01 & -1.01\\ -95 & 105 \end{pmatrix} \begin{pmatrix} 5 \\ 0 \end{pmatrix} = \begin{pmatrix} 0.5 \\ -47.0297 \end{pmatrix} \end{align*}

Buy \(0.5\) shares of the underlying and borrow \(\$47.0297\) in MMA at \(t=0\). The portfolio value at \(t=1\), in the cases the stock goes up and down, are \begin{align*} 0.5\times 105 - 47.0297\times 1.01 &= \$5,\\ 0.5\times 95 - 47.0297\times 1.01 &= \$0, \end{align*} respctively, which equal \(C_u\) and \(C_d\)

BOPM: Example (Cont..)

So far in the example, there is no physical probability \(p\) (because there is no need)

If an agent is confident the stock will go up (meaning the belief is the option price at \(t=1\) will be \(\$5\) with high probability \(p\)), and quotes \(C=\$4\) at today (\(t=0\)), how can you arbitrage?

Short sell the option to the agent to get \(\$4\) and spend \(\$2.970297\) to set up the replicating portfolio today. Your net cash inflow is \(4-2.970297 = \$1.029703\) at \(t=0\)

At \(t=1\), your obligation as an option writer (seller) is to pay the agent \(\$5\) if the stock goes up, and \(\$0\) if the stock goes down

But at \(t=1\), the replicating portfolio value is \(\$5\) if stock goes up and \(\$0\) if it goes down

In either case, you can liquidate the portfolio to fullfill your obligation

You are left with free cash inflow of \(\$1.029703\) at \(t=0\)

BOPM: Example (Cont…)

If the stock price did go up at \(t=1\) as expected by the agent, you pay the agent \(\$1\), as you sold the option at time \(t=0\) at the price \(\$4\) and buy it back at time \(t=1\) at the price \(C_u = \$5\)

But you still get to keep your risk free cash flow of \(\$1.029703\) at \(t=0\)

If you think this is a win-win situation as no one gets hurt, you are wrong

The agent could have made \(\$2\) by quoting the option at \(\$3\)

There is still room (\(3-2.970297 = \$0.029703\)) for arbitrage, and the market players will be happy to make the risk free profit

BOPM: Exercise

What’s the time zero PV of an ATM call option in BOPM with \(S = K = 100\), \(K\) the strike price, and \(S_u = 103\), \(S_d = 97\), \(M=1.01\)?

At \(t=0\), how many shares should you hold and how much money should you put in your MMA in order to set up a replicating portfolio?

Universal Option Pricing Formula

We’ve seen in BOPM that option price is a discounted expectation in the risk-neutral probability

This is true in general, regardless of the model (assumptions) used for the option pricing

Let \(X\) be any European payoff, a function of the underlying. Then the option price \(C\) is \begin{align*} C = M_0 \widetilde E[M_T^{-1} X] \end{align*}

An option pricing model specifies a distribution of the underlying (among other things) in the risk-neutral probability \(\widetilde P\)

Given the distribution, \(C\) is simply an integral

Change of Numeraire

The universal pricing formula \begin{align*} C = M_0 \widetilde E[M_T^{-1} X] \end{align*} is a special case of an even more general result

When we say \(S=\$100\) that means \(100\) USD, or \(100\) units of MMA

Any tradable asset can be used to denominate the underlying of the option

Examples are annuity and ZCB

“The underlying is trading at how many units of the annuity?”

The tradable asset used to denominate the underlying is known as the numeraire

Each numeraire is associated with a so-called equivalent martingle measure

The risk-neutral probability a special case of the equivalent martingle measure when using MMA as the numeraire

Let \(N_t\) be the numeraire used in option pricing, and the corresponding equivalent martingle measure is \(P^N\), then the time zero option price is \begin{align*} C &= N_0 E^N[N_T^{-1} X] \end{align*}

Change of Numeraire (Cont.)

The universal pricing formula \begin{align*} C = M_0 E^M[M_T^{-1} X] = N_0 E^N[N_T^{-1} X] \end{align*}

If you change a numeraire, you change the probability measure, and the distribution of the underlying

In fact, sometimes that’s the reaosn we change the numeraire: In the risk-neutral measure the distribution under some model is not known in closed form, but the distribution is known in closed form in a different measure so we can write the expectation as an integral

We will see example in SOFR caps and floors and swaptions pricing

An option pricing model can also specify a distribution of the underlying (among other things) in any equivalent martingle measure

SOFR Swaption

A swaption gives the holder the right, but not the obligation, to enter into a swap with a predetermined fixed rate (the strike) in the future

A 1y10y payer swaption with strike \(4\%\) is the right to enter into a 10y payer swap, with fixed rate \(4\%\), 1 year from now

1y is the expiry, or maturity, of the swaption

10y is the tenor

The end date of a 1y10y swaption will be 11y from now

Both parties are looking at the forward starting 10y swap with fixed rate \(4\%\), which starts 1y from now

If, at expiry, the spot starting 10y swap rate is higher than \(4\%\), say it’s \(5\%\), then the holder will exercise the option and enter into the payer swap

The holder will recieve floating coupons and pay \(4\%\) fixed coupons, at the end of every year, for the following 10 years

The holder then can enter into a spot starting receiver swap at \(5\%\), receiving \(5\%\) fixed coupons while paying floating

The net cash inflow is a \(1\%\) fixed coupon at the end of every year for 10y

If, at expiry, the spot starting 10y swap rate is lower than \(4\%\), then the option expires worthless

Forward Starting Swap PV Clean Form (Review)

Consider a tenor structure

\[T_0 < T_1 < T_2 < \cdots < T_N, \qquad \tau_n = T_{n+1} - T_n\quad \forall n=0, 1, 2, \ldots, N-1,\]where \(\tau_n\) is fixed to be 1Y

The time-\(t\) PV of an \(N\)-year-long forward starting payer swap with fixed rate \(K\) is \begin{align*} &\sum_{n=0}^{N-1}\left(\tau_n P(t, T_{n+1})L(t, T_n, T_{n+1}) - \tau_n P(t, T_{n+1})K\right)\\ =& \left(\sum_{n=0}^{N-1}\tau_n P(t, T_{n+1})\right)\left(\frac{\sum_{n=0}^{N-1}\tau_n P(t, T_{n+1})L(t, T_n, T_{n+1})}{\sum_{n=0}^{N-1}\tau_n P(t, T_{n+1})} - K\right) \\\\ =& A(t)(S(t) - K) \end{align*}

Here \(K\) is the strike \(4\%\) in the previous example

The forward starting swap rate \(S(t)\) fixes at \(S(T_0)\) to become the spot starting swap rate (\(5\%\) in the previous example)

Swaption Payoff

As explained earlier, if \(S(T_0) > K\) then the holder will exercise the payer swaption and if not, the option expires worthless

If \(S(T_0) > K\), the holder will enter into the swap with a nonzero initial NPV

\[A(T_0)(S(T_0)-K)\]Thus the payer swaption payoff is

\[X = A(T_0)(S(T_0)-K)^+\]which is a function of the underlying \(S(T_0)\)

This payoff makes annuity \(A(t)\) the natural choice of the numeraire for swaption pricing

Swaption Pricing

Payer swaption payoff

\[X = A(T_0)(S(T_0)-K)^+\]Payer swaption PV at time \(t\) \begin{align*} C &= A(0)E^A[A(T_0)^{-1} X]\\ &= A(0)E^A[(S(T_0)-K)^+] \end{align*}

From here we will need to specify a model, including a distribution of \(S(T_0)\)

The simpliest choice is the normal distribution \(N(0, \sigma^2T_0)\), which is the Black Normal model

SOFR Caps and Floors

Consider a tenor structure

\[T_0 < T_1 < T_2 < \cdots < T_N, \qquad \tau_n = T_{n+1} - T_n\quad \forall n=0, 1, 2, \ldots, N-1,\]where \(\tau_n\) is now fixed to be 3M

A 3M SOFR cap with strike \(K\) pays the buyer a series of cash flows

\[\tau_n(L(T_{n+1}, T_{n}, T_{n+1}) - K)^+ \quad\text{ at }\quad T_{n+1}, \quad \forall n=0, 1, 2, \ldots, N-1,\]where \(L(T_{n+1}, T_{n}, T_{n+1})\) is the SOFR term rate

Similarly, a 3M SOFR floor with strike \(K\) pays the buyer a series of cash flows

\[\tau_n(K - L(T_{n+1}, T_{n}, T_{n+1}))^+ \quad\text{ at }\quad T_{n+1} \quad \forall n=0, 1, 2, \ldots, N-1\]

Why the Name

Imagine you have liabilities to pay floating coupon \(\tau_n L(T_{n+1}, T_n, T_{n+1})\) every quarter (3M)

The payment to be made is unknown until the end of every coupon period, \(T_{n+1}\)

If you buy a cap with \(K = 6\%\), when the term rate fixes to be lower than \(6\%\), from the cap you recieve nothing:

\[\tau_n(L(T_{n+1}, T_n, T_{n+1}) - K)^+ = 0\]Given the liability, you will pay a lower than \(6\%\) coupon rate: \(\tau_n L(T_{n+1}, T_n, T_{n+1})\)

But if the forward rate fixed to be larger than \(6\%\), from the cap you recieve

\[\tau_n(L(T_{n+1}, T_n, T_{n+1}) - K)^+ = \tau_n(L(T_{n+1}, T_n, T_{n+1}) - K)\]Given the liability, you still pay a the coupon \(\tau_n L(T_{n+1}, T_n, T_{n+1})\)

Overall you pay \(\tau_n K\) which is at \(6\%\) annual coupon rate

If you buy a \(6\%\) cap, your payment is capped at \(6\%\) annual rate